In the world of both service and manufacturing industries where its development now uses equipment and material for transactions with communication and interaction media using electronic instrument instrument equipment such as AM, e-Money and currency transactions on the money market electronically as well as the emergence of digital currencies in the Finance technology equation this all requires a good knowledge of basic financial basics and calculations as well as the basic foundation of a qualified knowledge of electronic processes so that we know the process of financial transactions for the care and control of all financial transactions. in the financial world there are two well-known business transaction processes, namely working capital credit transactions and investment credit transactions, these two business characteristics that determine a company profit or loss on a micro scale as well as macro. while in the world of electronics as a counter and accelerating process and process security also creates many transactions and the value of money also adds wealth and prosperity in a country in a micro and international world on a macro basis, in control electronic transactions and instruments calculated by digits of more precise transactions and storage transaction process that can be stored for a long time; thus at a glance the process of growth of financial electronics for the time being that enables prosperity and the completeness of the processes of working capital and investment transactions .

LOVE ( Line On Victory Endless )

( Gen. Mac Tech Zone e- FIN WORK CAP & INVEST CAP )

What is the Electronic?

Electronics is the branch of science that arrangements with the investigation of stream and control of electrons (power) and the investigation of their conduct and impacts in vacuums, gases, and semiconductors, and with the device using such electrons.

This control of electrons is proficient by devices that resist, carry, select, steer, switch, store, control, and exploit the electron.

This control of electrons is proficient by devices that resist, carry, select, steer, switch, store, control, and exploit the electron.

The Future on WORKING CAPITAL

Working capital” is a measure of both a company’s efficiency and its short-term financial health. It generally is defined as current assets (e.g., cash, marketable securities, accounts receivable and inventories) minus current liabilities. The composition of working capital gives investors insights as to a company’s underlying operational efficiency. To illustrate, money tied up in inventory or money that customers still owe the company cannot be used to pay off any of the company’s obligations. Therefore, if a company is not operating in the most efficient manner (e.g., slow collections or low inventory turnover), the financial statements will report an increase in working capital.

Companies that improve the performance of their working capital can generate cash and see benefits far beyond the finance department.

Managing a company’s working capital isn’t the sexiest task. It’s often painstakingly technical. It’s hard to know how well a company is doing, even relative to peers; published financial data are too high level for precise bench marking. And because working capital doesn’t appear on the income statement, it doesn’t directly affect earnings or operating profit—the measures that most commonly influence compensation. Although working capital management has long been a business-school staple, our research shows that performance is surprisingly variable, even among companies in the same industry (exhibit). Working capital can amount to as much as several months’ worth of revenues, which isn’t trivial. Improving its management can be a quick way to free up cash.

For healthy companies, the windfall can often be reinvested in ways that more directly affect value creation, such as growth initiatives or increased balance-sheet flexibility. Moreover, the process of improving working capital can also highlight opportunities in other areas, such as operations, supply-chain management, procurement, sales, and finance. Of course, not all reductions in working capital are beneficial. Too little inventory can disrupt operations. Stretching supplier payment terms can leak back in the form of higher prices, if not negotiated carefully, or unwittingly send a signal of distress to the market. But managers who are mindful of such pitfalls can still improve working capital by setting incentives that ensure visibility, collecting the right data, defining meaningful targets, and managing ongoing performance.

Modify metrics to elevate visibility

Working capital is often under managed simply because of lack of awareness or attention. It may not be tracked or published in a way that is transparent and relevant to employees, or it may not be communicated as a priority. In particular, working capital is often under emphasized when the performance of a business—and of its managers—is evaluated primarily on income-statement measures such as earnings before interest, taxes, depreciation, and amortization (EBITDA) or earnings per share, which don’t reflect changes in working capital.

What actions should managers take, beyond communicating that working capital is important? In our experience, the selection of metrics to manage the business and measure performance is especially important, because different metrics will lead to different outcomes. For one manufacturing company, switching from EBITDA to free cash flow as a primary measure of performance had an immediate effect; managers began to measure cash flow at the plant level and then distributed inventory metrics to frontline supervisors. As a result, inventories quickly fell as managers, for the first time, identified and debated issues such as the right level of stocks and coordination among plants.

A disadvantage of free cash flow as a metric is that it may promote shortsighted decisions or excessive risk taking, such as reducing inventory to dangerously low levels to hit an end-of-period target. Tracking capital charges instead offers a more balanced incentive. For example, one engineering-services company added a capital charge for outstanding accounts receivable to the measure of account profitability it used to determine compensation levels for its sales force. That enabled account managers to better understand the real cost of working capital and see the rewards for what were sometimes painful calls to customers to collect late payments.

Collect the data

Many companies don’t systematically track or report granular data on working capital. That almost always indicates an opportunity to improve. For example, if managers at a manufacturing company can’t quickly determine how many days their current inventory will last at each location and stage of production—raw materials, work in progress, and finished goods—then they can’t be managing it well. If they don’t have readily available data on how much they spend with each supplier and their respective payment terms, then they aren’t managing accounts payable closely. Moreover, without such data, they may also be making erroneous decisions elsewhere. For example, after an audit of accounts payable at one company uncovered missing items and duplications , managers realized that different parts of the organization had been contracting the same suppliers without coordinating the process centrally through the procurement function. As a result, procurement managers had underestimated how much the company overall was spending with some suppliers by as much as 90 percent and thus had missed an opportunity to negotiate better volume discounts and payment terms.

Getting such data into a consistent and usable format the first time can be tedious, drawing from multiple legacy systems or breaking inventory down by production stage. Repeating that process manually isn’t practical—indeed, we’ve seen more than one company’s efforts to improve working capital falter when the process of gathering the data was too demanding to execute on an ongoing basis. Ideally, managers should build data collection into their core IT processes. Those who can draw on a single integrated system to automate the process will have an easier time of it. But managers who clearly identify the kind of data they need and where to get it can do quite well with a standardized template built into an Excel spreadsheet, which takes much less work to fill in as the process becomes routine.

Set more meaningful targets

Even when data are available, managers often set performance targets that affect working capital in a less-than-analytical way. We’ve seen many inventory managers, for instance, create target levels based on gut feel rather than calculating stocks based on observed variability. And we commonly observe companies setting incremental goals for improvement—by a few days or a few percentage points over their previous year’s performance.

More successful managers of working capital start by re-creating business processes as if there were no constraints and explicitly testing their assumptions—a so-called clean-sheet approach. For example, managers at a global manufacturing company had long held an average of 60 days’ inventory of a critical raw material at a certain plant to ensure that disruptions to supply wouldn’t affect production. When asked to improve that performance, they set an initial goal of cutting supply back to 50 days, a back-of-the-envelope improvement target arbitrarily based on their best performance in the past; they viewed this as quite aggressive.

In this case, that approach still would have left the company with unnecessarily high inventory levels, but without solid analysis, it could just as easily have been too aggressive. Fortunately, managers decided to test their assumptions using a clean-sheet approach. They calculated how much inventory they would need in a perfect world if there were no variability in the process. Then they added a buffer based on actual variability they had observed in demand and supply. In the end, they determined that they only needed to keep 30 days’ inventory. The 20-day gap between the incremental target and the clean-sheet target was worth tens of millions of dollars annually.

It’s important to note that the finance function should not set these targets on its own. Rather, it should involve operations managers, who can also take the lead on improvement initiatives. In many cases, excess inventory is driven by specific operational issues—for example, low reliability in one stage of a multistep manufacturing process. Target setting should also be a collaborative process that involves procurement (for accounts payable) and sales (for accounts receivable); those functions typically bear most of the burden of implementing improvements to working capital that are related to payment terms and collection.

While the full range of specific analytical tools is beyond the scope of this article, managers can make considerable headway by focusing on those areas of working capital with the largest dollar values, estimating clean-sheet targets, and then focusing on those places with the largest gap between incremental and clean-sheet targets. Areas of opportunity will differ by business, but in our experience, many companies find value in each: inventory, accounts payable, and accounts receivable.

Maintain momentum

Once companies have the basic incentives, data, and targets in place, they can turn to more advanced techniques for working capital management, such as supplier financing (particularly when a company’s cost of capital is lower than its suppliers’) and vendor-managed inventory. But many companies can wrest much of the value of working capital management just by maintaining the momentum of their baseline programs—to prevent them from eroding as time passes.

Insights from analysis of working capital can also be used to improve performance across a broad range of functions other than finance. Inconsistent customer terms and conditions brought to light by programs to improve the management of working capital, for instance, could signal an even bigger opportunity in pricing. The supply-chain data needed to manage working capital can reveal waste and inefficiency. For example, once they were reviewing data from accounts payable, managers at one company realized they could combine cargoes of raw materials in a way that reduced shipping costs and allowed a smaller network of warehouses. Additionally, the process of calculating safety stocks can uncover underappreciated supply-chain risks and lead to the development of diversified supply options and other contingency plans.

Working capital is important and often under-managed. Improving its performance can generate cash to fund value-creating opportunities and reveal insights that improve other aspects of business performance.

Future World Fund

The fund targets better risk-adjusted equity returns than a traditional index strategy by incorporating ‘factors’ into index design, while also seeking to address the investment risks associated with climate change.

Future World Global Credit

An actively managed global credit fund designed for sterling-based investors, which aims to preserve and grow capital while providing income. The fund expresses conviction views on the long-term themes that changing our world, while aiming to have a positive impact on society and create a powerful incentive for companies to change their behaviour.

Future World Sustainable Opportunities Fund

The fund is a high-conviction expression of long-term themes, seeking to invest in sustainable opportunities that will shape both the investment industry and society for years to come.

A.XO Financial Innovation

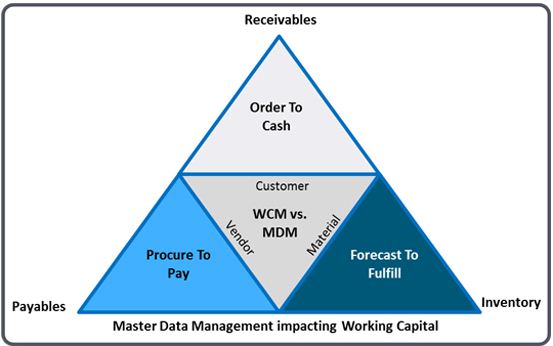

B. XO WORKING CAPITAL IN THE AGE OF DIGITAL FINANCE

“Working

capital, or free cash flow, is often seen as a quick barometer reading of a

company’s basic operating health.”

The point is that working

capital is the lifeblood of liquidity. If you have a poor working-capital

position, you will have trouble with liquidity, which will have a negative

impact on your business. In short, working capital is one of the key stability corporate , every CFO must

pay attention to.

But how can working capital be influenced?

The

most important areas influencing working capital are payables, receivables, and

inventory. Thus, collaboration between different departments – finance, purchasing

in accounts payable and inventory, sales in accounts receivable, production,

and certainly treasury – is also crucial. Besides that, highly automated

processes with real-time information also have a positive impact on working

capital .

companies that perform

better than their peers – the “leaders” – emphasize collaboration within the

company and beyond. The study also mentions that automation is a priority for

those CFOs, and that their core finance processes are extremely efficient. All

of these factors play an important role in maintaining working capital.

Companies need to get their cash cycle days, or the days of working capital

(DWC), as close to zero as possible. A simple calculation for DWC is days sales

outstanding (DSO) + days of inventory outstanding (DIO) – days payable

outstanding (DPO). The formula is quite simple, but to influence it, not so

much. As like as treasurers, real-time

information in the global cash and working capital situation is crucial. A

single version of the truth across all business units and entities will provide

immediate insight that enables them to evaluate appropriate actions. This

information is especially important for investment decisions – which will

ultimately have a significant impact on working capital. Working capital must

be and have to area of Finance and Controlling. This now we supporting companies in

their financial transformation and in designing their future finance IT

architecture and road map.

Factors affecting working capital requirements

- Nature of business,

- Size of business,

- Time and complexities of manufacturing process,

- Manufacturing cost,

- Growth and Expansion,

- Terms of purchase and sales,

- Conditions of supply,

- Market conditions,

- Business cycle,

- Operating cycle,

- Rate of Turnover,

- Cash requirements,

- Seasonal variations, and

- Other factors.

Debit card can be defined either in a simple way or detailed manner depending on how it is perceived with respect to different senses of finance. Following statements are few selected ones that lucidly express the definition of debit card within their individual perspectives. These definitions of debit card will help to get its overall understanding.

1. In a General sense,

“Debit card is a facility or utility provided by banking companies to their customers to help them execute (carry on, perform) different financial transactions anytime and anywhere that too with ease, comfort, speed and safety. Such a customer-friendly facility gives debit cardholders (users) a smarter and secured way to make quick payments while purchasing (i.e. during a sale transaction) various goods and/or services from any merchant (one that accepts a debit card) either from a traditional market or an online market.”

2. Within a Business perspective,

“Debit card is a suitable alternative to cash payment.”

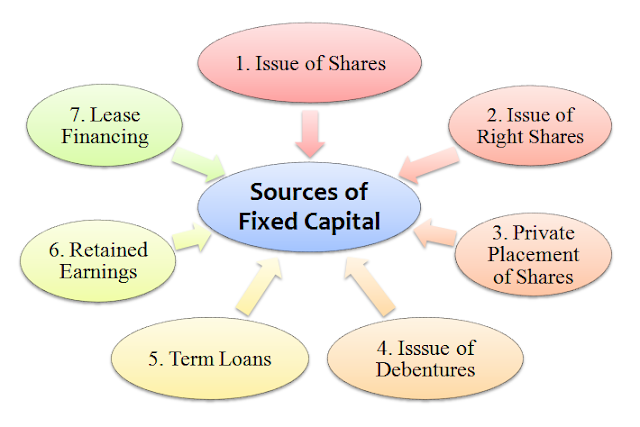

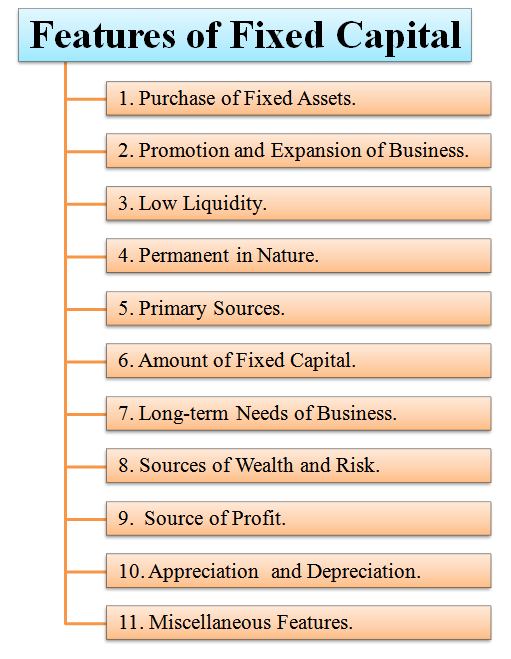

The sources of fixed capital or long term finance are:

- Issue of Equity and Preference shares.

- Issue of Right shares.

- Private placement of shares.

- Issue of debentures.

- Term loans.

- Retained earnings.

- Lease financing.

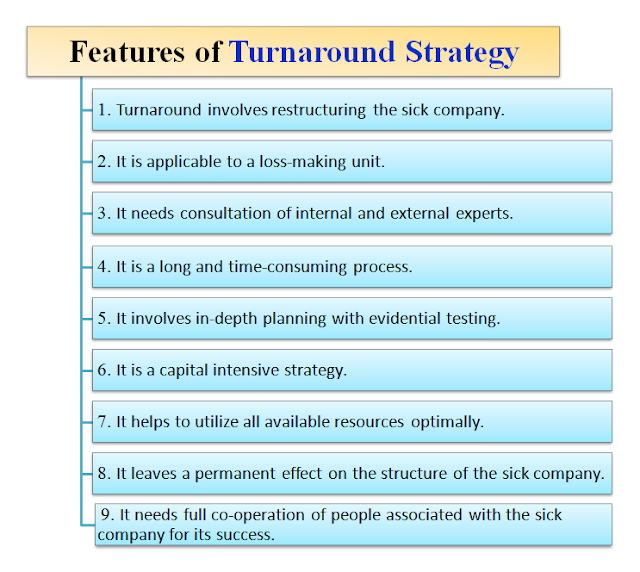

The concept or meaning of turnaround strategy covers following points:

- Turnaround strategy means to convert, change or transform a loss-making company into a profit-making company.

- It means to make the company profitable again.

- The main purpose of implementing a turnaround strategy is to turn the company from a negative point to a positive one.

- If a turnaround strategy is not applied to a sick company, it will close down.

- It is a remedy for curing industrial sickness.

- Turnaround is a restructuring strategy. Here, a loss-bearing company is transformed into a profit-earning company, by making systematic efforts.

- It tries to remove all weaknesses to help a sick company once again become strong, stable and a profit-making institution.

- It tries to reverse the position from loss to profit, from declining sales to increasing sales, from weakness to strength, and from an instability to stability.

- It aids to reduce the brought forward losses of the loss-making company.

- It helps the sick company to stand once again in the market.

- It is a complete U-turn of a planned strategic economic transition.

Priority sector plays an important role in the economic development of the country. Therefore, the Central (Federal) Government of any country gives this sector priority (first preference) in obtaining loans from banks at a low rate of interest. This is known as a ‘Priority Sector Lending’.

The classification or types of foreign collaboration include namely:

- Financial collaboration.

- Technical collaboration.

- Marketing collaboration.

- Management consultancy collaboration.

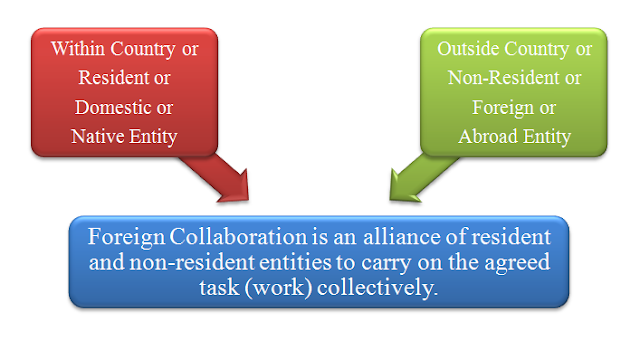

Definition of Foreign Collaboration

In general, the definition of foreign collaboration can be stated as follows.

“Foreign collaboration is an alliance incorporated to carry on the agreed task collectively with the participation (role) of resident and non-resident entities.”

Alliance is a union or association formed for mutual benefit of parties.

Foreign collaboration is such an alliance of domestic (native) and abroad (non-native) entities like individuals, firms, companies, organizations, governments, etc., that come together with an intention to finalize a contract on some tasks or jobs or projects.

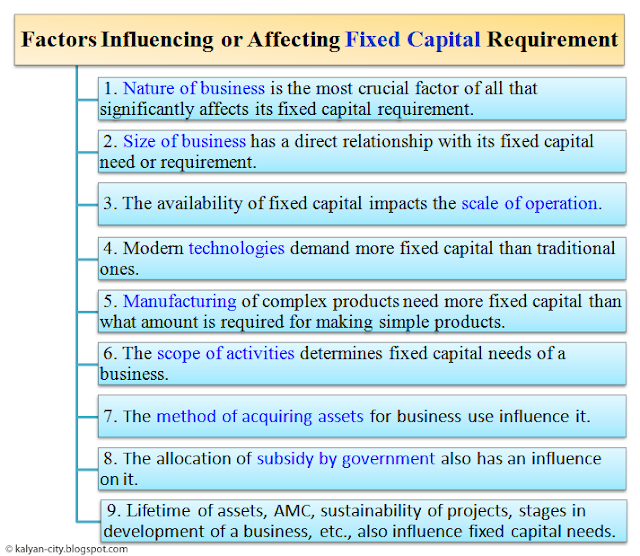

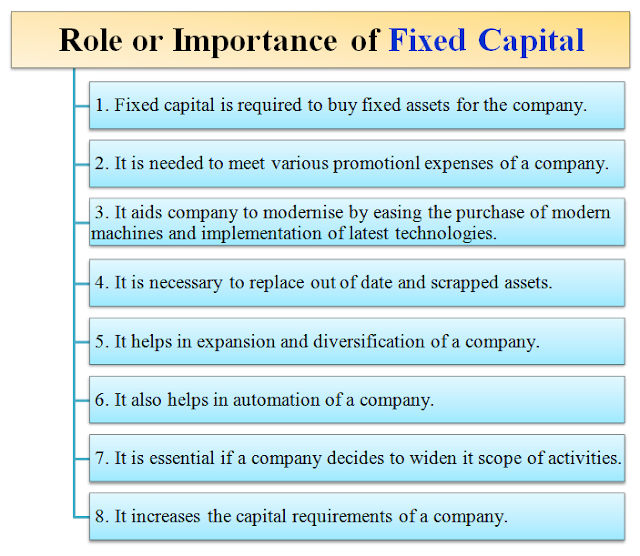

Fixed capital is a mandatory one-time investment made at the introductory phase of a business establishment.

Fixed capital is not alike working capital, which is required on a continuous basis to operate (run) the ordinary course of production and distribution of goods and services.

“Fixed capital is a compulsory initial investment made by the entrepreneur to start up the activities of his business.”

amalgamation can be stated as follows.

"Amalgamation is a union of two or more companies, made with an intention to form a new company."

In terms of finance, the definition of amalgamation can be given as under.

"Amalgamation is an agreement (deal) between two or more companies to consolidate (strengthen) their business activities by establishing a new company having a separate legal existence."

The definition of merger in general and in finance can be stated as follows:

In General,

"Merger is an absorption of one or more companies by a single existing company."

In Finance,

"Merger is an act or process of purchasing equity shares (ownership shares) of one or more companies by a single existing company."

C. XO Meaning of Investment

Meaning of Investment

In simple terms, Investment refers to purchase of financial assets. While Investment Goods are those goods, which are used for further production.

Investment implies the production of new capital goods, plants and equipments. We refers investment as real investment and not financial investment.

Investment is a conscious act of an individual or any entity that involves deployment of money (cash) in securities or assets issued by any financial institution with a view to obtain the target returns over a specified period of time.

Target returns on an investment include:

- Increase in the value of the securities or asset, and/or

- Regular income must be available from the securities or asset.

Types of Investment

Types of Investment

Different types or kinds of investment are discussed in the following points.

1. Autonomous Investment

Investment which does not change with the changes in income level, is called as Autonomous or Government Investment.

Autonomous Investment remains constant irrespective of income level. Which means even if the income is low, the autonomous, Investment remains the same. It refers to the investment made on houses, roads, public buildings and other parts of Infrastructure. The Government normally makes such a type of investment.

2. Induced Investment

Investment which changes with the changes in the income level, is called as Induced Investment.

Induced Investment is positively related to the income level. That is, at high levels of income entrepreneurs are induced to invest more and vice-versa. At a high level of income, Consumption expenditure increases this leads to an increase in investment of capital goods, in order to produce more consumer goods.

3. Financial Investment

Investment made in buying financial instruments such as new shares, bonds, securities, etc. is considered as a Financial Investment.

However, the money used for purchasing existing financial instruments such as old bonds, old shares, etc., cannot be considered as financial investment. It is a mere transfer of a financial asset from one individual to another. In financial investment, money invested for buying of new shares and bonds as well as debentures have a positive impact on employment level, production and economic growth.

4. Real Investment

Investment made in new plant and equipment, construction of public utilities like schools, roads and railways, etc., is considered as Real Investment.

Real investment in new machine tools, plant and equipments purchased, factory buildings, etc. increases employment, production and economic growth of the nation. Thus real investment has a direct impact on employment generation, economic growth, etc.

5. Planned Investment

Investment made with a plan in several sectors of the economy with specific objectives is called as Planned or Intended Investment.

Planned Investment can also be called as Intended Investment because an investor while making investment make a concrete plan of his investment.

6. Unplanned Investment

Investment done without any planning is called as an Unplanned or Unintended Investment.

In unplanned type of investment, investors make investment randomly without making any concrete plans. Hence it can also be called as Unintended Investment. Under this type of investment, the investor may not consider the specific objectives while making an investment decision.

7. Gross Investment

Gross Investment means the total amount of money spent for creation of new capital assets like Plant and Machinery, Factory Building, etc.

It is the total expenditure made on new capital assets in a period.

8. Net Investment

Net Investment is Gross Investment less (minus) Capital Consumption (Depreciation) during a period of time, usually a year.

It must be noted that a part of the investment is meant for depreciation of the capital asset or for replacing a worn-out capital asset. Hence it must be deducted to arrive at net investment.

Investment for E-Banking ? Online Banking ↓

E-banking refers to electronic banking. It is like e-business in banking industry. E-banking is also called as "Virtual Banking" or "Online Banking".

E-banking is a result of the growing expectations of bank's customers.

E-banking involves information technology based banking. Under this I.T system, the banking services are delivered by way of a Computer-Controlled System. This system does involve direct interface with the customers. The customers do not have to visit the bank's premises.

Popular services covered under E-Banking ↓

The popular services covered under E-banking include :-

- Automated Teller Machines,

- Credit Cards,

- Debit Cards,

- Smart Cards,

- Electronic Funds Transfer (EFT) System,

- Cheques Truncation Payment System,

- Mobile Banking,

- Internet Banking,

- Telephone Banking, etc.

Advantages of E-Banking ↓

The main advantages of E-banking are :-

- The operating cost per unit services is lower for the banks.

- It offers convenience to customers as they are not required to go to the bank's premises.

- There is very low incidence of errors.

- The customer can obtain funds at any time from ATM machines.

- The credit cards and debit cards enables the Customers to obtain discounts from retail outlets.

- The customer can easily transfer the funds from one place to another place electronically.

A financial plan is also called capital plan.

A financial plan is an estimate of the total capital requirements of the company. It selects the most economical sources of finance. It also tells us how to use this finance profitably. Financial plan gives a total picture of the future financial activities of the company.

Financial Planning is the mathematical sum of following parameters:

Financial Resources (FR) + Financial Techniques (FT) = Financial Planning.

A financial plan contains answers to the following questions:

- How much finance (short-term, medium-term and long-term) will be required by the company?

- From where this finance will be acquired (gathered)? In other words, what are the sources of finance? That is, owned capital (promoter contribution, share capital) and borrowed capital (debentures, loans, overdrafts, etc.).

- How the company will use this acquired finance? That is, application or utilisation of funds.

Financial plan is generally prepared during promotion stage. It is prepared by the Promoters (entrepreneurs) with the help of experienced (practising) professionals. The promoters must be very careful while preparing the financial plan. This is because a bad financial plan will lead to over-capitalization or under-capitalization. It is very difficult to correct a bad financial plan. Hence immense care must be taken while preparing a financial plan.

Types of Financial Plans

After the company starts, the finance manager does the financial planning.

The types of financial plans are depicted and briefly explained below.

There are three types of financial plans, viz.,

- Short-term financial plan is prepared for maximum one year. This plan looks after the working capital needs of the company.

- Medium-term financial plan is prepared for a period of one to five years. This plan looks after replacement and maintenance of assets, research and development, etc.

- Long-term financial plan is prepared for a period of more than five years. It looks after the long-term financial objectives of the company, its capital structure, expansion activities, etc.

Investment for Electronics Automated Teller Machine ↓

ATMs are electronic machines, which are operated by a customer himself to deposit or to withdraw cash from bank. For using an ATM, a customer has to obtain an ATM card from his bank. The ATM card is a plastic card, which is magnetically coded. It can be easily read by the machine.

To operate an ATM card, the customer has to inset the card in the machine. He has to enter the pass word (number). If the authentication or pass word (number) is correct, the ATM permits a customer to make entries for withdrawal or for deposit. On completion of the transaction, the customer's card is ejected from the ATM.

Advantages of Automated Teller Machines (ATMs) ↓

1. ATM provides 24 hours service

ATMs provide service round the clock. The customer can withdraw cash upto a certain a limit during any time of the day or night.

2. ATM gives convenience to bank's customers

ATMs provide convenience to the customers. Now-a-days, ATMs are located at convenient places, such as at the air ports, railway stations, etc. and not necessarily at the Bank's premises. It is to be noted that ATMs are installed off-site. (away from bank premises) as well as on site (installed within bank's premises). ATMs provide mobility in banking services for withdrawal.

3. ATM reduces the workload of bank's staff.

ATMs reduce the work pressure on bank's staff and avoids queues in bank premises.

4. ATM provide service without any error

ATMs provide service without error. The customer can obtain exact amount. There is no human error as far as ATMs are concerned.

5. ATM is very beneficial for travellers

ATMs are of great help to travellers. They need not carry large amount of cash with them. They can withdraw cash from any city or state, across the country and even from outside the country with the help of ATM.

6. ATM may give customers new currency notes

The customer also gets brand new currency notes from ATMs. In other words, customers do not get soiled notes from ATMs.

7. ATM provides privacy in banking transactions

Most of all, ATMs provide privacy in banking transactions of the customer.

Investment Of Concept quality

HOW IT WORKS (EXAMPLE):

Investments can be stocks, bonds, mutual funds, interest-bearing accounts, land, derivatives, real estate, artwork, old comic books, jewelry -- anything an investor believes will produce income (usually in the form of interest or rents) or become worth more.

WHY IT MATTERS:

The safety of the principal is of concern in any investment, although some investors are more risk tolerant than others and are thus more willing to lose some of their principal in return for the chance of generating a higher profit. The investor's ability to tolerate risk and the incremental return associated with increasing amounts of risk are two primary factors that distinguish types of investments from one another and help determine appropriate investments for a given investor.

it is important to understand these basic investment concepts.

Risk and return

Return and risk always go together. The higher the potential return, the higher the risk. You should never blindly pursue high-return investments. Bear in mind your investment goal, investment period and risk tolerance. Always choose an investment that is suitable for you.

Risk diversification

Any investment involves risk. You cannot avoid it, but you can manage your risk exposure with the right strategy to reduce the chances of major losses. The simplest and best way is to diversify your investments and spread your risk. An effective way is to diversify your investment to different asset classes, such as stocks, bonds, deposits etc.

Dollar-cost averaging

This is a long-term strategy. You regularly (e.g. monthly) invest a fixed amount, whatever the share price. In the long run this balances out the cost of buying shares and lessens the effect of short-term market fluctuation.

Compound Interest

Your principal (original money paid in) grows because of the interest earned, so you get a higher return. It’s a snowball effect – the longer you invest, the more you benefit from compound interest. Therefore, it is important to start saving and investing early.

Inflation

For the past few decades, there has usually been inflation in Hong Kong. Your investment needs a return rate that matches or beats inflation. If not, then your money will be worth less.

Significance Of INVESTMENT

Investment is the value of machinery, plants, and buildings that are bought by firms for production purposes.

Investment plays six macroeconomic roles:

1. it contributes to current demand of capital goods, thus it increases domestic expenditure; 2. it enlarges the production base (installed capital), increasing production capacity; 3. it modernizes production processes, improving cost effectiveness; 4. it reduces the labour needs per unit of output, thus potentially producing higher productivity and lower employment; 5. it allows for the production of new and improved products, increasing value added in production; 6. it incorporates international world-class innovations and quality standards, briging the gap with more advanced countries and helping exports and an active participation to international trade.

Composition

Although capital accumulation takes place in many institutional sectors of the economy (firms, households, public sector,…), a narrower definition is used in national accountancy.

Investment is just new capital accumulation in business (both private and state-owned).

Household by convention do not invest, even if it does exist a capital accumulation in cars, computers, electric appliances, etc. that we include in their "cumulative bundle".

Public expenditure is partly devoted to roads, railways, infrastructure, buildings (as for schools, hospitals,…). All this is clearly capital accumulation whose utility will last over time. Still, it is quite a common practice for investment in public sector being considered zero by convention.

Investment is classified according to the degree of directness with which it is linked to current and future sales:

1. inventories stock of finished goods, semi-manufactured goods, and raw materials in commercial premises, storehouses and producers' plants;

2. equipment for direct production of services and goods; 3. transport and auxiliary machineries; 4. office and general endowment for indirect workers and management; 5. any long-lasting improvement in those items; 6. industrial plants and service buildings; 7. other buildings.

In today's world, investment in immaterial assets is getting more and more important, as with the case of expenditure in Research & Development, human capital, software and other areas.

Financial investments in shares, obligations and other financial instruments are not considered as "investment" in a macroeconomic sense nor in national accountancy. The same is true for real estate exchanges of used buildings (both residential and non-residential).

When considering the issue of the creation and diffusion of innovation through investment, a crucial distinction should be made between complementary investments and competitive investments.

Determinants

At firm level, investment is determined by expected benefits as well as funds, both in term of availability and cost (interest rate).

Benefits relate to the effects of investment in terms of increased value added, reduced costs, larger production, higher competitiveness. Hence, profits are expected to be higher, too. The value over time of these benefits (and profits in particular) are compared to the investment costs.

The temporal profile of costs and revenues will be important in the decision whether to undertake the investment or not. In particulare the payback-period, in which the investment is covered by accrued profits, provides important reference for rules-of-thumbs.

In many decision processes and routines, the value over time of benefits will be discounted through a subjective discount rate to keep into account time distance and uncertainty. In others, the decision will be based on more strategic and vital arguments. A new vision of the competitive environment and of the global trends can bring to invest in surprising directions.

The prevailing conventions on time length of loans and bonds (5 - 10 - 15 - 20 - 30 years, with 50 or 100 being more unusual, except in certain countries or markets), coupled with payback periods of different types of investments across sectors and countries select and boost certain specific classes of investment instead of others.

This is because immediate profitability and coverage from stochastic variations of net benefits from an investment can be achieved by taking a loan for a period significantly longer than the payback period of the investment. In this way, the fixed payment per period becomes systematically lower than the net benefits, even during negative shocks. This mechanism, whose fine-tuning involves the level of interest rate, the mean, variance and auto-correlation of net benefits, is very powerful in boosting investment with short-term payback especially when interest rates are high and variance is high, depressing long-term investments.

Funds for investment can be obtained thanks to the following items:

1. self-financing, in turn due to:1.1. cumulated past profits;

1.2. injection of new financial capital from the owners; 1.3. amortization, i.e. accountancy allowance for past investment, considered now as current costs but not corresponding to any current expenditure; 1.4. extension of equity by new shareholders, as it happens with relatives sending remittances to home business;

2. loans from banks and other financial institutions:

2.1. long-term credit at fixed or variable interest rate in domestic or foreing currency; 2.2. short-term credit; 2.3. micro-credit in the case of very small business;

3. capital market finance, through the emission of obligations as well as through the issue of shares in the stock market (primary market). The following price fluctuation do not directly have any impact on financing the firm. But it is true that further new emissions of shares often require positively-oriented capital markets.

4. seed money and expansion capital for new firms provided by venture capitalists and private equity funds;

5. public funds and incentives for investment from international, national, regional, local institutions.

However, the empirical evidence of microdata shows that investment - at micro level - is infrequent and lumpy. There are periods in which firms decide not to invest and periods of large investment episodes. For better understand the issues at stake see this paper.

Investment expenditure is a bet on future. If the bet is lost, the product does not find a remunerative market and much of the investment expenditure turns out to be a sunk cost that cannot be recovered. In the extreme case, investment is irreversible. Coupled with true uncertainty, irreversibility becomes a fairly important determinant of investment levels across industries, as this paper points out.

In the IS-LM model, interest rates are considered the unique determinant of investment. In fact, interest rates play three distinct functions:

1. they influence the discounted value of net benefits over time;

2. they determine the cost of loans from banks and the required rate of return for the owners and financing institutions; 3. they set the economic climate both for financial and real markets.

In all three function, a higher interest should trigger a lower investment, since the present value of benefits will be lower, finance costs higher and economic perspectives worse.

Still, there exists investments that are not based on interest rates considerations. For instance, firms have usually a very restricted number of investment projects, carrying them out when profitability is well above zero. A small change in interest rate would have simply no impact on each investment decision, thus on aggregate level as well.

By contrast, the effect of large interest rate changes may be highly asymmetric: a strong increase of interest rate can indeed provoke a fall in investment dynamics whereas a similar decrease may fail to induce investment, if real perspective benefits are lacking.

Other determinants of investment should be considered as, for instance, present and expected consumption and export.

Saturation of productive capacity represent a key references for firms' decisions to invest. Expectations about future sales will affect investment if the current capacity is not enough to match the forecasted increase in demaned quantities and the firm is committed to fulfill all orders. Given a ratio of fixed capital to sales, the investment required would be (in a very simplified method of estimation) this ratio times the new additional expected sales.

Furthermore, new technology innovation and the need of imitating competitors' adoption of innovation can also force firms to invest, in a process of diffusion that can be boosted by a conducive tax environment, both in terms of tax breaks and pro-diffusion-of-innovation tax.

Investment in real estate new developments and rejuvenation of existing areas are better understood in operations like urban regeneration.

Cumulated investments over time give rise to capital, opening the path to improvements in production conditions.

Production capacity, potential productivity, cost effectiveness, production and process quality will be all increased by properly-oriented investment. Exportcompetitiveness should also rise.

Employment can fall if a labour substitution investment prevails with real output growing less than physical productivity. By contrast, other kinds of investment and economic situations give rise to an increasing employment. The quality and composition of employment also depend on the investment directions. For instance, green jobs significantly depend on wide investment in green sectors and technologies.

As a GDP component from the current domestic expenditure side, investment has an immediate impact on GDP. An increase of consumption rises GDP by the same amount, other things equal. Moreover, since income (GDP) is an important determinant of consumption, the increase of income will be followed by a rise in consumption: a positive feedback loop has been triggered (between consumption and income) by investment.

Because of this mechanism, imports will grow as well. More directly, investment is often directed to foreign machineries and goods, with an immediate increase of imports.

Countries differ a lot in respect to investment levels and dynamics. Some countries have heavily invested, sacrificing current consumption and triggering an export-led growth, often based on manufacturing. Others keep investment at much lower levels with an unsecure growth path.

A large-scale investment effort in clean technologies and processes is seen as a conditions for coping with climate change. The our book on "Innovative Economic Policies for Climate Change Mitigation" puts forth the proposal of a closed long-term fund to influence investment decisions of private and public bodies.

Business cycle behaviour

With its short and violent fluctuations, investment is a clear source of the business cycle.

During economic expansion, investment grow at a much faster pace than consumption or GDP, usually irrespective of interest rate movements.

On the contrary, the influence of interest rates on investment can be important at turning points. At peaks, consistent increase of the interest rate would drastically worsen the costs of existing loans for past investment. Disappointment from demand grow may combine with this effect to reduce investment dynamics.

Investment often peaks earlier than GDP, triggering a negative income-consumption multiplier, thus prompting a new recessionary direction.

At trough, low interest rates may be one of the very few good news for firms. Thus, combined with positive expectations, investment may start growing from the very low level at which they were.

Positive expectations toward the economy may also bring leading firms to invest earlier than the trough. In so doing they may even invert the business cycle.

On the other hand, investment in machinery may instead follow the lower trough, since the first recovery may simple use the existing, not-fully exploited capital.

Changes in government, with opposition going to the power, can exert an important effect on raising or abating the expectation of business in terms of the overall economic environment and for specific actions.

Needless to say, business cycles have many sources and paths, thus wide discrepancies with the previously presented scenario can arise.

|

Portfolio investment is considered to include securities transactions not belonging to direct investment and reserve assets. Portfolio investment refers to securities transactions in which the ownership or voting power after the investment remains below 10%. As securities transactions are valued at market prices, capital gains realised in connection with a change of ownership are reflected in valuation adjustments between stocks and flows.

Securities traded are divided into equity and debt securities. Equity securities are shares, participations and mutual fund shares. Debt securities include bonds and money market paper.

Income generated from mutual funds' share holdings are divided into profits (dividends) and reinvested earnings. Reinvested earnings are included in the security investments in the financial account while profits (dividends) are included in the primary income in the current account.

Data on security investments are collected in the inquiry on foreign financial assets and liabilities and from data collections carried out by the Bank of Finland. The Bank of Finland collects data by security and in their classification use is made of the European Central Bank's centralised database on securities, which contains basic data on nearly all securities under active trading globally.

Types of Investments

Think of the various types of investments as tools that can help you achieve your financial goals. Each broad investment type—from bank products to stocks and bonds—has its own general set of features, risk factors and ways in which they can be used by investors.

E.XO Electronic Methods of Communication in Business

As technology progresses, new communications are born and old ones--many of which seemed new not so long ago--fade away. When you're trying to connect with employees, colleagues, bosses, clients, customers, suppliers or any other business contact, you may have more choices than you realize. Whether for interpersonal or marketing communications, electronic media are critical to getting business done efficiently and cost-effectively.

Mobile Devices

Although communication with mobile devices may be less formal than other forms of communication, people are increasingly turning to text messages and short emails using cell phones and personal digital assistants (PDAs). Text messaging in particular has strong appeal, as anyone with a cell phone has texting capability. PDAs with Internet capability have changed the way email works, often turning it into a means of keeping in touch via short, quick messages--much like a text message but with use of a different connection type. As a result, not only do business associates communicate with one another via mobile devices, but many companies have begun marketing to customers through mass text messages.

Social Networking Media

The capability and uses of social networking media continue to evolve. Some maintain social networking represents a new frontier in marketing and business networking. Companies promote events, communicate with customers, offer discounts and draw attention to sales using social networking media. Recruiters and salespeople often seek key contacts through social media sites.

For example, recruiters may search for a chief financial officer (CFO) candidate by sifting through and connecting with CFOs who are listed on business social networking sites. This gives them a new way to reach people without having to get past secretaries or working hard to get private home phone numbers.

One of the older forms of electronic communication remains a staple of modern business. Because of its versatility, email can be used for asking questions and getting answers, holding mini-group conferences, making people aware of issues, passing along documents, sharing information and much more. Most courts now admit email as evidence and legal proof of contracts and transactions.

From a marketing standpoint, email has become a popular medium for sending messages to customers. For many companies, email blasts supplement and replace what used to be print direct mail. Now instead of getting a card in the mail about their favorite store's upcoming sale, customers receive graphically enhanced emails. Not only does this reach people directly, but email blasts help companies save on printing and mailing costs.

how real companies are winning each of these fights—overcoming inertia while building confidence about how to master the new economics of digital.

1. Fighting ignorance

Many senior executives aren’t fully fluent in what digital is, much less up to speed on the ways it can change how their businesses operate or the competitive context. That’s problematic. Executives who aren’t conversant with digital are much more likely to fall prey to the “shiny object” syndrome: investing in cool digital technologies (which might only be relevant for other businesses) without a clear understanding of how they will generate value in the executives’ own business models. They also are more likely to make fragmented, overlapping, or subscale digital investments; to pursue initiatives in the wrong order; or to skip foundational moves that would enable more advanced ones to pan out. Finally, this lack of grounding slows down the rate at which a business deploys new digital technologies. In an era of powerful first-mover advantages, winners routinely lead the pack in leveraging cutting-edge digital technologies at scale to pull further ahead. Having only a remedial understanding of trends and technologies has become dangerous.

Raising your technology IQ

For inspiration on how to raise your company’s collective technology IQ, consider the experience of a global industrial conglomerate that knew it had to digitize but didn’t think its leadership team had the expertise to drive the needed changes. The company created a digital academy to help educate its leadership about relevant digital trends and technologies and to provide a forum where executives could ask questions and talk with their peers. Academy leaders also brought in external experts on a few topics the company lacked sufficient internal expertise to address.

Supplementing the academy effort (aimed at leaders) was an organization-wide assessment of digital capabilities and an evaluation of the company’s culture. This provided a fact base, which everyone could understand, about what the organization needed to build over the course of the digital transformation. As business leaders developed digital plans, they were accountable for explaining and defending them to other executives. They also had to help gather those plans into an enterprise-wide digital strategy that every business leader understood and had helped to create.

Overcoming competitive blind spots

If your company resembles many we know, it’s still stuck in some old ways of thinking about where money gets made and by whom. You’re also likely to be overlooking ways digital is changing both the economics of the game and the players on the field in your industry. If any of this sounds familiar, you probably need a jolt—something that forces you to think differently about your business. More specifically, you need to start thinking about it as digital disruptors do. In our experience, this demands a process that begins with a sprint to get everything moving, to see what your industry (and your company’s role in it) could look like if you started from scratch, and to redraw your road map.

The financing division of a European financial-services company went through such a process when it tried to understand digital’s impact on its current lines of business. For example, a conversation began in the auto-loans division with the question “how can we make it easier for people to get their loans online?” It turned into a deeper examination of “how does our business model change if people stop buying cars and start buying mobility?” Similarly, an auto insurer might move from asking “how can I sell car insurance online better” to “what does car insurance mean in the context of autonomous vehicles?” There’s no substitute for exploring such questions, which emerge when digital, regulatory, and societal trends collide with today’s value chain

Once the new realities are discovered, companies should speed up the process of understanding how other players—including nontraditional ones—will respond. The financial-services provider jump-started things by holding a series of war-gaming workshops. It divided its leadership team into groups and assigned them to role-play potential attackers such as Amazon, Google, or small, cherry-picking start-ups. Seeing through the eyes of “baggage-free” attackers inspires an awareness of how players with very different core competencies are likely to act in the new landscape. It can also propel a shared sense of urgency to change the old ways of thinking and acting.

These sessions radically changed the way the company’s leaders thought about their business, their industry, and the digital shifts remaking both. The end result was a set of leading-edge ideas for deploying digital to make the current operating model faster and more effective, for investing in new digital offerings, for designing and launching a new digital ecosystem to meet the emerging needs of digital consumers, and for partnering with start-ups beginning to emerge as leading players in advanced mobility.

2. Fighting fear

Getting left behind by digital first movers can be hazardous to your company’s future. But many of your executives may perceive responding to digital—making the big bets, building new businesses, shifting resources away from old ones—as hazardous to their own future. As we’ve noted, that exacerbates the social side of strategy and breeds strategic inertia. If you want to make big digital moves, you must fight the fear that your top team and managers will inevitably experience.

From what we have seen, this kind of fight doesn’t happen organically. You need to design a programmatic effort with the same rigor you would insist on to redesign key processes across your organization. This typically involves making a clear case that executives can’t hide from the changes digital is bringing and that encouraging and accelerating change—rather than chasing it—can create more value. Then you need to give executives the tools and support network they must have to succeed as leaders of that journey. Many companies focus on the extensive detailing of digital-initiative plans but skip the critical step of building an equally rigorous program to sustain the leaders driving change.

Honest dialogue

At the industrial company we discussed earlier, the move to digital implied significant change in the characteristics leaders required to be effective. Naturally, concerns about waning influence, or worse, followed for many of the company’s 20 or so business-unit leaders. The industrial conglomerate confronted these fears head-on by organizing a top-team effectiveness program to surface anxieties, build awareness of how they were affecting decision making, and define how leaders could remain relevant. In workshops, executives discussed the specific mind-sets and behavioral shifts needed to gain “ownership” of digital initiatives as a group and to become role models for their organizations.

Support networks

Leaders also formed communities that cut across their businesses, initially to share best practices and coordinate the timing of implementation. Over time, the role of these communities grew to include skill-building activities, such as bringing in speakers with specialized capabilities and motivational messages and organizing Silicon Valley go-and-sees that reinforced the importance of leading digital change. The communities also provided peer support to help teams navigate the new landscape.

We have seen other organizations similarly coalesce around digital-leadership training (sometimes supported by digital advisory boards) that helps executives to become comfortable with—even embrace—the uncertainty of the destination and the career trade-offs needed for a well-executed digital strategy. These support networks dovetail with, and bolster, the digital IQ–raising efforts we described earlier. Indeed, we find that leaders who understand the shifting economics also understand that their careers will be affected one way or another.

3. Fighting guesswork

Pursuing an aggressive digital strategy involves leaps into the unknown: simultaneously, you are likely to be moving into new areas and overhauling existing businesses with new technologies. What’s more, in many digital markets, the premium of being a first mover makes it necessary not only to shift direction but also to do so faster than your peers. The combination of ambiguity and the need for speed sometimes gives rise to guesswork and moves that are hasty or poorly thought out—and to anxiety about whether a move isn’t going to work or just needs more time.

Building the proof points as you go

One way to fight guesswork is to anchor your strategy decisions to a thesis about the business outcomes that different digital investments will produce. This is less about elaborate business-school modeling and more about thinking that draws fast, ground-level lessons from the data to determine whether your business logic is correct. Put another way, it means figuring out if there is sufficient value to make it worthwhile to invest something—as part of a process of learning even more. This approach increases the odds of successful implementation: a well-articulated view of the outcomes means that you can track how well the strategy is working. It also makes it easier to assess whether the new direction is worth it in terms of both financial capital and organizational pain.

Those proof points must be grounded in digital reality. Consider the experience of a global oil and gas company investigating the potential impact of several advanced technologies on its business. Rather than develop theoretical value-creation scenarios, the company’s digital center of excellence got busy exploring: How might sensors, robots, and artificial intelligence improve productivity and safety in unmanned operations? What operating hurdles, such as skill gaps among managers and frontline workers, would need to be overcome?

“Skunkworks” efforts began to give the company sharper insights into the timetables and financial profiles of different investments, so it avoided both the “finger in the air” syndrome (which dooms some digital efforts) and excessive modeling (which bogs down others). The end result was a value-thesis projection of a pretax cash-flow improvement exceeding 20 percent by 2025. That built the confidence of senior leaders and the board alike.

Pilots and stage gates

A second way to reduce the need for guesswork is to take full advantage of real-time data and the opportunities they provide for experimentation. Digital does amplify the gut-wrenching uncertainty by multiplying the strategic choices leaders face while reducing the time frame for making and implementing those decisions. But it also contains a silver lining: the potential for gaining rapid, data-driven insights into how things are going. Information on the progress of a product launch, for example, is available in days rather than months. That makes rapid course corrections possible and, ultimately, considerably improves the chances of success.

The oil and gas company mentioned earlier got a rapid bead on the impact that its digital initiatives were having on its business performance when it automated the evaluation of several business cases. Testing was more or less continuous, which reduced the level of anxiety about the investments, because executives had hard data on how things were performing rather than relying on guesses or intuition in realms they didn’t know extremely well. It also gave them more confidence to push cutting-edge solutions: they didn’t need to see how other oil and gas companies did things when they could move first and see, in near real time, what worked and what didn’t.

An important element of this nimble approach was breaking up big bets into smaller, staged investments. While the oil and gas company was ready to invest in digital, it was decidedly uncomfortable with throwing money at a problem and hoping for the best. It therefore developed a series of rigorous stage gates for investments managed by a new, central digital-transformation office. The office was charged with overseeing the portfolio of digital investments to ensure that the most promising projects were funded and others defunded before they soaked up valuable resources. In tandem, the head of the company’s digital efforts was vested with the responsibility for approving which ideas would move to initial development, basing these decisions on the organization’s overall vision for digital.

The ideas, which originated mostly with the business units, included clear requirements for testing. The “fail fast” mind-set was embedded from the outset because it allowed the company to learn quickly from mistakes and to minimize wasted funding. Another payoff was that the central team could identify synergies, which allowed the development costs of some investments to be shared rather than borne by a single business. These processes helped temper some of the risks of the bold investments the company was making, gave leaders the confidence to venture ahead as first movers, and kept open the option to correct course quickly when the data pointed in another direction.

4. Fighting diffusion

Effective strategy requires focus, but responding to digital inevitably risks diffusion of effort, or “spreading the peanut butter too thinly.” Most companies we know are trying, and struggling, to do two things at once: to reinvent the core by digitizing and automating some of its key elements, for example, and to create innovative new digital businesses. The challenge is acute because of the dizzying pace of digital change and the uncertainty surrounding the adoption of new technology. Even if the technology for autonomous vehicles pans out, for instance, when will the majority of people really begin to use them? Given the impossibility of knowing, it’s easy to wind up with an unfocused hodgepodge of digital initiatives—a far cry from a strategy.

Two concepts can help you navigate. First, view your company as a portfolio of initiatives at different stages of seeding, nurturing, growing, or pruning. Our colleague Lowell Bryan championed this view upward of 15 years ago, and it is more relevant than ever in our digital age because the opportunities, time frames, and economics of core businesses can be very different from those of new ones—so resources and efforts shouldn’t be applied uniformly.

Second, embrace the necessity of “big moves,” such as the dramatic reallocation of resources, sustained capital investment, radical productivity improvements, and disciplined M&A. As our colleagues have shown, successful market-beating strategies nearly always rest on such moves. Making them mutually reinforcing, so that developments in the core help to support new digital businesses and vice versa, is a critical part of managing the risks of diffusion.

To understand what the application of these ideas looks like in practice, consider the experience of a global IT-services company wrestling with how much to invest in digital over the next five years (rather than use standard R&D funding across all of the company’s business lines). That meant scrutinizing which traditional businesses faced obsolescence as a result of digital, whether digital could stretch any of those lifetimes (or if immediate divestment was preferable), which new digital businesses to invest in, and how much to invest.

A portfolio approach

As a first step, the company went through its portfolio business by business, focusing on three questions: Which emerging digital products and services were missing from the portfolio? Which product offerings and elements of the existing operating model should be digitized or fully digitally reengineered to improve customer journeys? And what areas should be abandoned? The answers for the company’s healthcare markets differed from those for banking, but the company became comfortable with hard choices and more attuned to new opportunities by tying all decisions to clear use cases.

As part of this exercise, the company developed scenarios for how the value pools in each of its industry verticals would probably shift across component customer value chains. It wanted to get a sense of the types of services that clients and potential clients were likely to demand and thus might try to obtain from new suppliers or IT outsourcers. For businesses where more revenue would be likely to shift, the company was comfortable placing bigger bets on new digital offerings, in contrast with its approach to businesses where the revenue at stake wasn’t changing as much.

Big, mutually reinforcing moves

This systematic evaluation of value-pool opportunities across the portfolio generated a frank discussion of how the organization’s risk appetite had to change. It also catalyzed a greater willingness to invest in new digital businesses—which the company did, to the tune of more than $1.5 billion. As part of this strategic evolution, the company launched an aggressive program to better leverage foundational digital capabilities, such as automation, advanced analytics, and big data. These capabilities, to be sure, were key building blocks for the new digital businesses. Just as important, however, by deploying the capabilities at scale across existing businesses, the company was better able to stretch the life of its core offerings.

The portfolio strategy paid dividends both in revenue gains and cost reductions. For example, investing in a balanced fashion between core and new businesses led to faster than expected revenue streams from new offerings. The company estimated that 40 percent of its revenues would flow from them within two to three years. Moreover, its digitally improved core businesses, with a sizable base of existing customer revenues, provided additional funding for the new digital portfolio. That increased the leadership’s commitment to the strategy, bolstering confidence that the new portfolio offerings would provide growth more than compensating for the eventual decline of core businesses.

Your best digital competitors—the ones you really need to worry about—aren’t taking small steps. Neither can you. This doesn’t mean that a digital strategy must be designed or put to work with any less confidence than strategies were in the past, though. Strategy has always required closing gaps in knowledge about complex markets, inspiring executive teams (and employees) to go beyond their fears and reluctance to act, and calibrating risks when you bet boldly.

The good news is that the digital era, for all its stomach-churning speed and volatility, also serves up more information about the competitive environment than yesterday’s strategists could ever imagine. Simultaneously, analytically backed, rapid test-and-learn approaches have opened up new avenues to help companies correct course while staying true to their strategic goals. Today’s leaders need to step up by persuading their organizations that digital strategies may be tougher than other strategies but are potentially more rewarding—and well worth the bolder bets and cultural reforms required, first, to survive and, ultimately, to thrive.

Capabilities at scale

For digital success, certain capabilities—especially those that build foundations for other key processes and activities—are more important than others. Foremost among them are the modular IT platforms and agile technology-delivery skills needed to keep pace with customers in a fast-moving, mobile world. The IT platforms of most companies we surveyed have major gaps, reflecting (and reinforced by) a widespread failure to prioritize digital initiatives within broader IT and capital-expenditure investments.

What further separates high performers in our survey is their ability to engage customers digitally and to improve their cost performance in four areas.

Data-empowered decision making

High-performing digital companies distinguish themselves by keeping pace as their customers undertake the digital consumer decision journey. For example, they anticipate emerging patterns in the behavior of customers and tailor relevant interactions with them by quickly and dynamically integrating structured data, such as demographics and purchase history, with unstructured data, such as social media and voice analytics. These companies skillfully assess the available resources, inside and outside the business, and bring them to bear on issues that matter to their markets.

Connectivity

A closely related skill is connectivity. Digital leaders embrace technologies (such as apps, personalization, and social media) that help companies establish deeper connections between a brand and its customers—and thus give them more rewarding experiences. Such connections can also deeply inform product development.

For example, Burberry’s Art of the Trench campaign, launched in 2009, encourages customers to visit its online platform and upload photographs of themselves in trench coats. Fellow shoppers and fashion experts then comment on the photos and “like” and share them through email, as well as social-media outlets. Users can also click through to the main Burberry site to shop and buy. These innovations are becoming ever more deeply embedded in the company.7Burberry may not have gotten everything right, but, overall, this approach—combined with other innovations—helped the company to double its annual total revenue in six years.

Process automation

Top-performing digital players focus their automation efforts on well-defined processes, which they iterate in a series of test-and-optimize releases. Successful process-automation efforts start by designing the future state for each process, without regard for current constraints—say, shortening turnaround time from days to minutes. Once that future state has been described, relevant constraints (such as legal protocols) can be reintroduced.

Using this approach, a European bank shortened its account-opening process from two or three days to less than ten minutes. At the same time, the bank automated elements of its mortgage-application process by connecting an online calculator to its credit-scoring models, which enabled it to give customers a preliminary offer in less than a minute. This system cut costs while significantly improving customer satisfaction.

Two-speed IT

Today’s consumer expectations put a new set of pressures on the IT organization as legacy IT architectures struggle with the rapid testing, failing, learning, adapting, and iterating that digital product innovations require. Our diagnostic shows that leading companies can operate both a specialized, high-speed IT capability designed to deliver rapid results and a legacy capability optimized to support traditional business operations.

This IT architecture and, in certain cases, the IT organization itself essentially function at two different speeds. The customer-facing technology is modular and flexible enough to move quickly—for instance, to develop and deploy new micro services in days or to give customers dynamic, personalized web pages in seconds. The core IT infrastructure, on the other hand, is designed for the stability and resiliency required to manage transaction and support systems. The priority here is high-quality data management and built-in security to keep core business services reliable.

financial institution used this two-speed approach to improve its online retail-banking service. The bank opened a new development office with a start-up culture—an agile work process tested and optimized new products rapidly. To support this capability for the long term, the company simultaneously evolved its service architecture to accelerate the release of new customer-facing features.

A fast, agile culture

While strong skills are crucial, companies can to some degree compensate for missing ones by infusing their traditional cultures with velocity, flexibility, an external orientation, and the ability to learn.

These test-and-learn approaches incorporate automation, monitoring, community sharing, and collaboration to unify previously isolated functions and processes into a fast-moving, product-oriented culture. By promoting shared ownership of technology initiatives and products, such environments democratize data, minimize complexity, facilitate the rapid reallocation of resources, and enable reusable, modular, and interoperable IT systems.To set this kind of culture in motion, executives can focus their efforts on four key areas.

External orientation

As companies develop their collaborative cultures, they position themselves to participate more meaningfully in broader networks of collaboration, learning, and innovation. The shaping role in these networks, or ecosystems, may be beyond the reach of most incumbent companies. But they can play other value-creating roles by performing specific modules of activity, such as production or logistics, within a more broadly orchestrated ecosystem.

Collaboration beyond the boundaries of companies need not occur only in a broadly orchestrated setting. Companies can also benefit from smaller-scale collaborations with customers, technology providers, and suppliers. In addition, they can mobilize workers they themselves don’t employ—the distributed talent in networks of shared interest and purpose. SAP, for instance, mobilized the user community it developed to help launch its NetWeaver software.

All this requires digital leaders to recognize what they’re good at themselves and what others might do better and to improve their ability to partner collaboratively with people and institutions. They must also be able to separate the real opportunities, threats, and emerging collaborators and competitors from hype-laden pretenders.

Appetite for risk

The research finds that digital leaders have a high tolerance for bold initiatives but that executives at laggards say their cultures are risk averse. Although established companies may not be likely to shape or orchestrate broad ecosystems, they must still face up to the implications of disruptive forces in their markets and industries—and the risks that arise in dealing with them. In a world of more data and less certainty, companies have to make decisions and respond to disrupters all the earlier and the more decisively.

Test and learn—at scale!

At the heart of agile cultures is the test-and-learn mind-set and product-development method, which can usefully be applied, or translated, to nearly any project or process that incumbents undertake. Instead of awaiting perfect conditions for a big-bang product launch or deferring market feedback until then, digital leaders learn, track, and react by putting something into the market quickly. Then they gauge interest, collect consumer reactions, and pursue constant improvements. Rigorous data monitoring helps teams quickly refine or jettison new initiatives, so that such companies fail often and succeed early.

Internal collaboration

Teamwork and collaboration are important in any context, digital or otherwise. Wharton’s Adam Grant says the single strongest predictor of a group’s effectiveness is the amount of help colleagues extend to each other in their reciprocal working arrangements.

F. XO Improving Working Capital Management Processes

In best-practice organizations, working capital improvements are driven by customer-centric strategies.

measures and monitoring are fundamental to the change process. Sample working capital benchmarks include:

- Return on Capital

- Working Capital as Percent of Sales

- Days Sales Outstanding

- Percent Past Due

- Invoice Error Rate

- Days Inventory Outstanding/Inventory Turns

- Days Payable Outstanding

- Procurement Card Percentage of Spend