e- SWITCH DOLLAR ( electronics@Short Wave Interaction To Couple Highway Direct Online Love Liquid And Redial )

several analytical theories of observing the payment of money transactions electronically to decide a project progress :

1. The time series experiment

2. The equivalent time samples design transactions e- money

3. The equivalent composition sell and buy transaction design

4. The non - equivalent control group design

5. Counterbalanced transaction e- money design

6. The separate sample before and past transaction e- money

7. The separate sample before and past control group and instrumentation e- money

8. The multiple time -series e- money transaction

9. The re-current cycle design of e-money Transaction

10. Regression - discontinuity analysis

11. Correlational and ex post facto design decision maker from e- money Transaction

Payment Method Selection

If users have no way of paying you, they have no way of buying anything from you, and so it’s clear that accepting a wide range of payment methods is a good idea to ensure that all users actually have a way of sending money your way.

How to Design Payment Method Selection

So how should the payment method selection be designed? There isn’t one “right” design as it depends on the number and types of payment methods accepted, as well as the rest of the checkout design. However, while there isn’t one “right” solution there are a number of principles to follow when designing the payment method selection in your checkout process:

- Place the options in close proximity so the user can see all the available payment methods in a single view, allowing them to compare the options and make an informed decision about which one to choose.

- Make it absolutely clear which option is currently selected – the user must never be in doubt about which payment method that’s currently active.

- Use progressive disclosure to gradually reveal form fields so the user only sees form fields relevant to the current selection(s).

- Explain the different payment methods and highlight their most important implications (e.g. “1% fee when paying with American Express” or “product only shipped once bank transfer clears”) so the user can make an informed decision about which option is the most appropriate to them.

- Consider having a default selection to speed up form entry and reduce choice paralysis by nudging users towards a particular payment method (typically the most popular one).

Why Accepting Numerous Payment Methods Is Important

As mentioned in the introduction, accepting a wide range of payment methods is important – first and foremost because users quite simply won’t be able to buy anything from you if you don’t accept the payment methods they have at their disposal. It’s obvious but absolutely critical. The solution of course is to make sure you accept a sufficiently wide range of payment methods to avoid shutting the door in the face of potential customers – although this is easier said than done, especially in the case of international e-commerce sites.

The number of payment methods that should be accepted will tend to increase along with the number of countries that are catered to, as some countries will require one or more local payment methods to be accepted due to unique local payment infrastructures and customer preferences.

There are additional benefits outside pure and simple “transaction ability” to supporting multiple methods, the three most significant supplementary advantages being:

- Redundancy – The more payment methods you accept, the more redundancy there will be in your payment system should one of them break down temporarily (as pretty much all systems eventually do at some point) or have to be taken down for maintenance. In these instances, if you have a wide range of payment methods, you can temporarily disable the malfunctioning one while it gets fixed, without having your entire store coming to a grinding halt.

- Preference – Users may prefer certain payment methods over others for any number of reasons, ranging from fee structures to privacy concerns to how secure they believe the option to be. Users will therefore often appreciate having a choice so they can pick their preferred payment method, even if they would be able to buy with another one had it not been available to them.

- Fallback – It’s not just your systems that can fail, the user’s payment instruments may stop working too, whether it temporary (such as credit card declines due to valid but unusual card activity, unbalanced accounts, technical issues with their provider, etc) or permanently (expired cards, closed accounts, etc). In these cases, being able to pay with a wider range of payment methods will allow the user to fall back on one of their other (working) payment options - see this article on how we recoup up to 30% of all declined transactions.

There’s of course a wide variety of payment methods, some of which change the nature of how, where and when the transaction takes place. Much the same way that customers have payment preferences, e-commerce sites may have them too. It should be a mix of these site and user needs and preferences that determine which types of payment methods to implement first in the face of resource constraints. Let’s look at the characteristics of the most common types of payment methods:

{{% table %}}

| Payment Method | Benefits | Challenges |

|—————-|———-|————|

| On-site credit card payment – the user enters their credit card details directly at the site.

| Payment Method | Benefits | Challenges |

|—————-|———-|————|

| On-site credit card payment – the user enters their credit card details directly at the site.

Example: Gilt, “Credit card” fields |

- Full control over transaction and user experience

- Most users are accustomed to this flow

- Supporting local credit card types (e.g. going beyond Visa, Amex, MasterCard and Discover)

- Legal and technical PCI compliance

| 3rd-party checkout – the user checks out at an external site such as PayPal, Wallet, or Alipay.

Example: Walmart “PayPal” |

- Easy way to support a wealth of local payment methods

- Some users prefer these solutions due to privacy, checkout simplicity, or unused account credits

- Little control over the user experience

- Some services require users to sign up for an account

- It's often not possible to determine what customer data to capture, and some providers don't share all data collected

| Invoice and wire transfer – the user receives an invoice and pays by making a wire transfer.

Example: Buy.com “Pay by wire transfer” |

- Many B2B and B2G users have no other payment method

- Making the technical and logistical distinction between orders with instant vs delayed payments

| Gift cards, coupons and other credits – the user pays with a type of store credits.

Example: Kohl’s “Gift card(s)”, “Kohl’s cash”, “Promo code(s)” |

- Enables loyalty programs, customer segmentation, price differentiation, etc

- Site abandonments and lower margins due to "coupon hunting"

- Often subject to partial funds, requiring multiple payment methods to be combined

| Financing – the order is financed by a 3rd-party intermediary.

Example: Apple “Financing” |

- Gives users without the sufficient funds a way to purchase

- Financing commission

- Abandonments during the credit approval process

- Potential delay due to credit approval

| By phone – the user calls in and provide their payment options over the phone.

Example: Barnes & Noble “Pay by phone” |

- Easier and more reassuring for novice users

- Phone capacity

| Using multiple cards or payment methods – the user combines multiple payment methods to pay for their order.

Example: HP “Pay with more credit cards” |

- Allows the user to overcome any credit limits or account balance variations by distributing the order total across multiple payment methods

- Complex user interface

- Legal and technical PCI compliance

E.T. can't phone home (and vice-versa) without something called a graphics processing unit (GPU), a specialized circuit that accelerates the processing speed of electronic devices. Crypto-miners, gamers and alien hunters all require GPUs for their purposes, but the latter two groups claim there's been a shortage since the bitcoin blitz.

"We'd like to use the latest GPUs ... and we can't get 'em," Dan Werthimer, chief scientist at Berkeley Search for Extraterrestrial Intelligence (Seti) Research Center, told the BBC on Wednesday.

"That's limiting our search for extraterrestrials," he added.

SETI, a global program devoted to searching for signs of extraterrestrial civilization, listens to radio channels for traces of alien broadcasts. The task requires tons of processing power, with some of Berkeley SETI's telescopes requiring as many as 100 GPUs.

XO__XO The Future of Electronic Payments

The actual definition of an electronic payment is simple: when you transfer money from one account to another electronically, i.e., without the need for paper checks or currency notes. Examples include making online bill payments; direct debits and credits in your bank account; tax refunds and other government disbursement into your bank account; and using credit and debit cards in online stores.

Sounds straightforward enough, until you consider the many types of electronic payments and the concerns they raise. Get started with this look at how electronic payments have evolved, and how they might look in the future.

The First Electronic Payments

Some payment mechanisms have been around much longer than others. The earliest versions of modern-day credit cards existed even in the mid-20th century. The first forms of electronic payments were motivated by the need for efficient alternatives to paper-based payments, primarily for business-to-business transactions, but with e-commerce, electronic payments are the only practical option.

Even as recently as the late ‘80s, several of the EFT (Electronic Fund Transfer) platforms were primarily used for B2B banking. Today, that’s changing, because a significant proportion of the globe’s population has access to at least one of the following: a credit card, online access to their bank account, a stored value online account, or the like.

Types of Electronic Payments Popular Today

If you have made a payment without handing over some form of paper – currency notes, checks, coupons – then you likely made an electronic payment. The most common types include:

- Credit and Debit Cards: These are the most popular electronic payment tools. While a credit card gives you a convenient loan for purchases, a debit card withdraws money from your bank account. Given their popularity, no business owner can afford to reject credit cards as a form of payment.

- RFID Cards: Some toll passes, such as E-ZPass, allow you to automatically pay as you drive past a tollbooth. These RFID (radio-frequency identification) cards “talk” to a receiving device at the tollbooth and make the payment. The greatest attraction of RFID cards is they process transactions without the need for physical contact – no swiping, no tapping. Especially in high-speed locations, such as a tollbooth, nothing can match the convenience of an RFID card.

- Online Bank Payments: When you transfer money to someone else’s account, or pay a utility bill from your account, you’re making an online bank payment. For many, bank accounts are the primary payment facilitators. Even if you use some other form of payment, you likely need to associate it with a bank account.

- Electronic Checks: These did not get as popular as some predicted. Electronic checks are just the online version of paper checks. They require a digital signature, and are governed by the same regulations that govern paper checks. Its similarity to a paper check makes an electronic check attractive, but people expect electronic payments to be much faster. Electronic checks aren’t much faster, and that prevent them from becoming too popular.

- Online Stored Value Accounts: Stored value accounts such as PayPal have become quite popular because the convenience—you can receive payment based solely on an email address. Of course, if you want to add or withdraw money from your account, you need to link it to a credit card or bank account.

- Digital Wallets: A digital wallet is a device, or application on a device such as a mobile phone, that either stores money or can withdraw money from a credit card or bank account. They enable customers to store information for multiple cards, making it more convenient to pay when shopping online or on a mobile device, beacause you don’t have to enter card information for every purchase. Examples include Apply Pay, Google Wallet and Softcard. Versatility makes digital wallets a major electronic payments innovation.

- Smartcards: Smartcards are the new generation of plastic. Instead of a magnetic strip, your information is stored in a microchip, which enables greater functionality. In many cases credit card issuers have upgraded the plastic of all cardholders. This has caused smartcards to become a common payment method overnight. Widespread usage, coupled with a much higher degree of security, has motivated businesses to upgrade their swipe machines to accept smartcards too.

What’s the Catch? Electronic Payments Aren’t Without Challenges

- Security: The upside of electronic payments is that they are more efficient than manual methods. The downside is that if left unchecked, they can also lead to efficient payment frauds! If all you need to authenticate a transaction is a device or credit card numbers, then someone might very well be able to withdraw money from your account.

- Privacy: To transact, electronic payment mechanisms store your information. Users fear that this information could be misused.

- Connectivity: To authenticate and complete an electronic transaction, you need an Internet connection. Places with poor connectivity can’t easily adopt electronic payment systems.

- Inclusion: Underlying most electronic payment mechanisms is a bank account. For the part of the population not eligible for a bank account, this is a deterrent.

The Future of Electronic Payments: What to Expect in 2015 and Beyond

- Stronger Security: Today we can configure a foolproof authentication system. But the problem with very high levels of security is that they make transactions cumbersome. For instance, you could take a thumbprint scan every time you use your digital wallet. But in addition to delaying each transaction, this process would require a fingerprint scanner. Every year, we are making greater strides in security. Encryption technologies, including SSL (Secure Sockets Layer), are now commonplace. Several online payment options require multifactor authentication too.

- Smarter Credit Cards: How smart can a credit card be? A smartcard could easily enable parents to block mobile app purchases by their kids, while permitting other purchases. Until then, present-day technology permits all your credit cards to be loaded on to one smartcard, doing away with the need to carry a wallet full of plastic.

- Biometric Payments: What if at a checkout counter, all you had to do was press your thumb to a scanner, and the money would automatically be taken from your credit card or bank account? It’s technologically possible today, and many researchers support biometric authentication. But the necessary backend infrastructure is not in place to make this option widely available—yet.

- Mobile Payments: While mobile phone-based payments rely on a credit card or bank account, they may do away with the need to carry that piece of plastic. Using the NFC (Near Field Communication) technology in your mobile device, you can get authenticated, and money can be withdrawn from your account.

Electronic payments are rapidly evolving, and the future is looking to bring more convenience and security than ever before.

Future of Money: Classifying Virtual Currency Systems

Since the beginning of the digital age, pundits have hailed virtual currencies as the future of our civilization’s money. While it may be difficult to imagine a cash-less society, it’s important to understand that money is merely an agreement to use something as a medium of exchange. The function and purpose of cash is therefore assigned by our cultural and social systems, not any intrinsic value. So as our society evolves, and our physical and digital economies converge, how does our monetary system evolve along with us? Whether exchanged via virtual worlds, social games, or mobile apps, virtual currencies hold real implications for our global economy, fundamentally altering how we conduct transactions with one another.

Technological advancement has coincided with currency reform throughout human history. The advent of writing in early Mesopotamia provided new ways to number commodities, forming the basis of accounting. Machine-minted coin production in the industrial age brought England out of a reliance on precious bimetals and towards a sustainable monetary system. And the personal computer of the information age enabled more convenient transactions through e-commerce and credit card processing. We now find ourselves in a hyper-connected digital world, with start-up entrepreneurs and corporate giants all competing to shape the manner in which we exchange 21st century goods and services.

To better understand the virtual currency landscape, we might observe four broad trends emerging: mobile fiat currency, corporate value currency, virtual world currency, and peer to peer currency. Although the nuances of these categories may blend together, I draw distinctions at their core function -- why and how the currency is created, circulated, and adopted.

Mobile Fiat Currency

Mobile fiat currency allow consumers to send and transfer legal tender using their mobile phone. With Square, people can pay by swiping a credit card through a plug-in device on the iPhone. Similarly, Pay Pal’s Card.io app scans a credit card number using nothing but the phone’s camera. Other platforms, like Google Wallet, Zong, and Isis, invest in “Near Field Communication (NFC)” technologies, which enable consumers to tap their smartphone on a reader to complete a transaction. Yet because NFC relies on consumers carrying NFC enabled phones, merchants installing NFC equipment, and complex alliances with various stakeholders, it will take time for “wave and pay” to reach mass adoption.

To really see mobile payment in widespread practice, look no further than Africa, where the lack of credit card penetration has brought mobile innovation to the forefront. One popular service called M-Pesa sends funds via text messages. Customers hand over cash to any one of thousands of participating retailers. They are then credited virtual money on their phone, which can be dispersed through SMS or exchanged back for cash at any time. As of 2010, 9.5 million people subscribe to M-Pesa and collectively transfer the equivalent of 11% of Kenya’s GDP each year.

Another type of mobile fiat currency involves “carrier billing,” whereby a consumer pays using their phone number (rather than their credit card number), and the charges are billed directly to their phone bill. By linking your phone to your Pay Pal account, you can do things like book a hotel room in under 60 seconds or buy a friend a beer with a tweet. With these services, companies stand to profit from even more frictionless payments than we have now.

Corporate Value Currency

Corporate value currencies are rewards or credits that are acquired by engaging with a company or participating in a loyalty program. There are numerous examples -- Shopkick’s Kickbucks announce deals to consumers as soon as they enter a store; GetGlueprovides entertainment discounts to people who “check-in” to the shows they watch. Corporate value currencies are often associated with the gameification movement, helping people quantify their progress and unlock new achievements. Denominated in points, credits, mileage, and badges, these currencies are inextricably tied to a company's product or service, rather than any official tender. Their value, then, has to do with demonstrating mastery, redeeming prizes, and earning freebies.

Facebook Credits, the universal currency for buying social games and applications on Facebook, has integrated with traditional promotions and deals. When you make purchases at restaurants or retailers, you can now have Facebook credits automatically deposited in your account. Facebook and American Express even have a partnership that lets users pay for exclusive virtual goods in Farmville by using their American Express Membership points. These corporate value currencies work because people perceive their value as higher than their cost. In reality, Facebook Credits cost next to nothing, about $0.10 each. But with 5.8 million people playing FarmVille and 90.6 million playing CityVille every month, Credits have become more desirable and meaningful than a standard store coupon.

Virtual World Currency

Virtual world currencies circulate within internal virtual world communities. Accumulating fictional money helps improve one’s experience of the game, whether that be by acquiring accessories, weapons, land, or $330,000 space stations. In 2009, Americans spent $620 Million dollars in the virtual world industry. Second Life, one of the largest virtual world platforms, collected $144 million in Q2 of 2009, a higher GDP than 19 countries. These massively-mutiplayer-online games (MMOPGs) are usually based off subscription fees or virtual goods sales and are designed primarily for leisure, play, and entertainment.

Buying virtual goods signal players' social standing, showcases their virtual identity, and opens more doors for experience. Yet in-game currency takes time to earn. In World of Warcraft, “virtual workers” spend long hours performing monotonous tasks in order to accumulate gold, level up their characters, and sell the avatars for real money. Such “gold farming” raked in an estimated $3.0 billion dollars in 2009, indicating how virtual world currencies can turn into real money profits.

Peer to Peer Currency

Peer to peer currency is driven by networked communities and serve as an alternatives to centralized bank currency. It has gained momentum alongside Local Exchange Trading Systems (LETS) and time banks, which have provided complimentary currencies for the past 30 years. The most notable digital form of currency is Bitcoin, a system operated by computing networks that collectively encrypt, verify, and process transactions, almost like a Bittorrent for cash. Bitcoin has distinct advantages over banks - it’s open source, non-national, always available, stable in supply, and policed by its users rather than an organization. At the same time, a security breach in summer 2011 compromised hundreds of accounts and led to the theft of approximately $500,000 dollars worth of virtual money. Since then, Bitcoin’s biggest challenge has been to regain public confidence in its security and sustainability.

Peer to Peer currencies approach how they store value in different ways. The pricing of Ven rises and falls based on a basket of currencies, commodities, and carbon components rather than being tied to a single currency like the dollar. Ripple, a decentralized open source payment method, positions everyone as a banker; people issue credit to each other based on real-life relationships. Once again, the goal is to shift ownership of money away from centralized banks and towards everyday citizens.

Other peer to peer communities trade, swap, and barter goods and services without a medium of exchange. These “collaborative consumption” platforms range from housing, to skills, to free time, to recyclables. Swap.com is the largest of these communities, facilitating trade of over 1.5 million personal items. While there are advantages to standardized currency, collaborative consumption holds tremendous environmental promise, helping people save money, save resources, and strengthen a community through sharing.

The Future of Money

What other forms of money might we see? We may be headed towards a system that converts personal and social data into online currency. Companies today quantify and commoditize our online activity for free, but that may not always be the case, especially as start-ups develop “personal data lockers” for people to store information about themselves. If the technology takes off, we might imagine a future in which users trade their personal data to advertisers in exchange for something of value in return.

Of course, virtual currencies and e-commerce platforms have risen and fallen faster than consumers have had time to adopt them. As Microsoft’s former CTO Nathan Myhrvold prognosticated in a 1994 Wired article: "Today we have a zillion different ways of doing financial transactions. There's cash, checks, credit cards, debit cards, wiring money, traveler's checks ... each of these has a particular point. We're going to see that much diversity in digital money." Indeed, each type of virtual currency affords unique advantages and disadvantages for specific situations. It is a future not of digital money, but of digital monies, and to shape it, we need to better understand where our money system has been, where it is now, and where we would like it to go next.

2017 has been the year of issuing tokens on top of Ethereum, and one of the more intriguing tokens recently announced is Tether, which is backed by U.S. dollars in a bank account. However, there is an issue with this token that makes it unlikely to stand the test of time, at least in its current form.

What is Tether?

The basic concept behind Tether is quite simple. An entity holds U.S. dollars in a bank account and then issues Tether tokens based on that bank account balance. One Tether is equal to one US dollar.

The first version of Tether was issued on top of the Bitcoin block chain by way of the Omni protocol, and there is currently over $430 million worth of Tether on the network . With Omni, users are able to issue digital assets in a manner similar to the popular ERC-20 tokens seen on Ethereum.

Before creating Ethereum, Vitalik Buterin worked on the Omni project — although it was called Mastercoin back then.

Governments around the world will undoubtedly try to clamp down on the use of digital currencies for illicit purposes at some point in the future. And this clampdown may happen sooner rather than later with the alleged use of bitcoin by North Korea to get around various sanctions placed upon it by the United States and others.

Last week, U.S. Senator Ed Markey called for Bitcoin to be “shut off” (either entirely or just from North Korea) on CNN.

Of course, the point of Bitcoin is that it is supposed to be able to avoid censorship from governments. This same logic does not apply to Tether. The central point of failure for Tether is the bank account where all of the actual US dollars that back the token are stored.

Without real U.S. dollars to back it, Tether would have no value. Putting U.S. dollars on a blockchain does not remove the central point of failure that backs them.

So what will happen when governments decide to target Tether? The best place to look for guidance here may be the cases of Liberty Reserve and E-gold. When these centralized virtual gold currencies were being used for illicit purposes and the companies backing them did not implement the proper tools to track payments and holdings to real-world identities, they were shut down.

So, either the code that controls the Tether tokens on Bitcoin and Ethereum will need to be updated to track payments or the bank account backing the token will be seized.

In the case where the Tether token is updated, those who do not identity themselves will most likely not be able to send their tokens to anyone else or redeem them through Tether directly (this is how the process worked when E-gold was shut down), making them worthless. Even if a Tether user is willing to identify himself in order to claim his money, those funds will likely be unavailable to him during the legal proceedings following the shutdown.

If Tether does not comply with regulators, they’ll likely face the same fate as Liberty Reserve and E-gold.

This is Why Bitcoin is Not Threatened by Fiat Virtual Currencies

The potential regulatory issues around Tether illustrate the value proposition of bitcoin. Satoshi Nakamoto’s creation exists because any form of true digital cash must be resistant to censorship from attackers (governments or otherwise). If someone can shut down the Bitcoin network, then the intrinsic value of bitcoin is lost.

Recently, BTCC CEO Bobby Lee gave a presentation in New York where he discussed the properties of bitcoin and how they differentiate the cryptocurrency from various forms of fiat-based virtual currencies.

As I’ve written in the past for Nasdaq, there should be an opportunity for bitcoin to succeed as the world becomes increasingly digitized and governments do not want to relinquish their ability to track payments, seize assets, and inflate the money supply. Digital gold.

The initial coin offering (ICO) craze is getting ridiculous. The latest evidence: A cryptotoken called “Useless Ethereum Token” has raised over $40,000 in just under three days.

Here’s its pitch: “UET is a standard ERC20 token, so you can hold it and transfer it. Other than that… nothing. Absolutely nothing.” And the offering still has four days to go before it closes.

Useless Ethereum Token is part caustic satire, part artistic intervention. Its anonymous creator, who goes by UET CEO, told the New York Observer: “I realized that people didn’t really care about the product. They cared about spending a little bit of money, watching a chart and then withdrawing a little bit more money. So why not have an ICO without a product, and do so completely transparently just to see what happened?”

Indeed, token offerings have already raised $327 million in the first half of the year, according to research by trade publication CoinDesk. That doesn’t account for monster raises in the interim, like the EOS offering, which attracted over $200 million worth of ether in about two weeks, according to research firm Smith and Crown.

UET is not the only gag cryptocoin. Another newly launched one is FOMO Coin, which promises a remedy to speculators with a fear of missing out on the next hot ICO. “Get in before it’s too late!” its website exhorts readers. “We’ve been working on FOMO Coin for at least two hours.” FOMO Coin has only attracted $6.50 in ether so far.

FOMO Coin’s creator, a software developer in Ireland named Jamie Farrelly, told Quartz he had indeed only worked on it for a couple of hours. “It’s a real token, I had a few hours to spare,” he said. “Plus the current ICO situation is nuts. Had to make people think a bit more about it.”

Joke coins have a history of taking on a life of their own in the cryptocurrency world. Just look at dogecoin, the granddaddy of humor-based cryptocurrencies. The “doge” in question is a Shiba Inu dog named Kabosu who was photographed looking askance at the camera, an image that then transmogrified into a viral meme. In 2014, as bitcoin was becoming exposed to the mainstream for the first time, a community sprung up online to create a cryptocurrency inspired by the meme. It raised $30,000 for the Jamaican bobsled team to compete in the winter Olympics.

But that wasn’t the end of it. Since then, dogecoin’s value has risen about 20-fold, to a high of over $400 million for all the dogecoin in circulation in June—and that’s despite the fact that no one has touched its code for about two years. Joke coin investors are laughing all the way to the bank.

Compare study for Electronic Transactions on numerical analysis

Electronic Transactions on Numerical Analysis

Electronic Transactions on Numerical Analysis (ETNA) is an electronic journal for the publication of significant new developments in numerical analysis and scientific computing. Papers of the highest quality that deal with the analysis of algorithms for the solution of continuous models and numerical linear algebra are appropriate for ETNA, as are papers of similar quality that discuss implementation and performance of such algorithms. New algorithms for current or new computer architectures are appropriate provided that they are numerically sound.

Stock dilution

Stock dilution, also known as equity dilution, is the decrease in existing shareholders’ ownership of a company as a result of the company issuing new equity. New equity increases the total shares outstanding which has a dilutive effect on the ownership percentage of existing shareholders. This increase in the number of shares outstanding can result from a primary market offering (including an initial public offering), employees exercising stock options, or by issuance or conversion of convertible bonds, preferred shares or warrants into stock. This dilution can shift fundamental positions of the stock such as ownership percentage, voting control, earnings per share, and the value of individual shares.

Control dilution

Control dilution describes the reduction in ownership percentage or loss of a controlling share of an investment's stock. Many venture capital contracts contain an anti-dilution provision in favor of the original investors, to protect their equity investments. One way to raise new equity without diluting voting control is to give warrants to all the existing shareholders equally. They can choose to put more money in the company, or else lose ownership percentage. When employee options threaten to dilute the ownership of a control group, the company can use cash to buy back the shares issued.

The measurement of this percent dilution is made at a point in time. It will change as market values change and cannot be interpreted as a "measure of the impact of" dilutions.

- Presume that all convertible securities are convertible at the date.

- Add up the number of new shares that will be issued as a result.

- Add up the proceeds that would be received on these conversions and issues (The reduction of debt is a 'proceed').

- Divide the total proceeds by the current market price of the stock to determine the number of shares the proceeds can buyback.

- Subtract the number bought-back from the new shares originally issued

- Divide the net increase in shares by the starting # shares outstanding.

Earnings dilution

Earnings dilution describes the reduction in amount earned per share in an investment due to an increase in the total number of shares. The calculation of earnings dilutions derives from this same process as control dilution. The net increase in shares (steps 1-5) is determined at the beginning of the reporting period, and added to the beginning number of shares outstanding. The net income for the period is divided by this increased number of shares. Notice that the conversion rates are determined by market values at the beginning, not the period end. The returns to be realized on the reinvestment of the proceeds are not part of this calculation.

Value dilution

Value dilution describes the reduction in the current price of a stock due to the increase in the number of shares. This generally occurs when shares are issued in exchange for the purchase of a business, and incremental income from the new business must be at least the return on equity (ROE) of the old business. When the purchase price includes goodwill, this becomes a higher hurdle to clear.

The theoretical diluted price, i.e. the price after an increase in the number of shares, can be calculated as:

- Theoretical Diluted Price =

Where:

- O = original number of shares

- OP = Current share price

- N = number of new shares to be issued

- IP = issue price of new shares

For example, if there is a 3-for-10 issue, the current price is $0.50, the issue price $0.32, we have

- O = 10, OP = $0.50, N = 3, IP = $0.32, and

- TDP = ((10x0.50)+(3x0.32))/(10+3) = $0.4585

If the new shares are issued for proceeds at least equal to the pre-existing price of a share, then there is no negative dilution in the amount recoverable. The old owners just own a smaller piece of a bigger company. However, voting rights at stockholder meetings are decreased.

But, if new shares are issued for proceeds below or equal to the pre-existing price of a share, then stock holders have the opportunity to maintain their current voting power without losing net worth.

Market value of the business

Frequently the market value for shares will be higher than the book value. Investors will not receive full value unless the proceeds equal the market value. When this shortfall is triggered by the exercise of employee stock options, it is a measure of wage expense. When new shares are issued at full value, the excess of the market value over the book value is a kind of internalized capital gain for the investor. He is in the same position as if he sold the same % interest in the secondary market.

Assuming that markets are efficient, the market price of a stock will reflect these evaluations, but with the increase in shareholder equity 'management' and prevalence of barter transactions involving equity, this assumption may be stretched.

Preferred share conversions are usually done on a dollar-for-dollar basis. $1,000 face value of preferreds will be exchanged for $1,000 worth of common shares (at market value). As the common shares increase in value, the preferreds will dilute them less (in terms of percent-ownership), and vice versa. In terms of value dilution, there will be none from the point of view of the shareholder. Since most shareholders are invested in the belief the stock price will increase, this is not a problem.

When the stock price declines because of some bad news, the company's next report will have to measure, not only the financial results of the bad news, but also the increase in the dilution percentage. This exacerbates the problem and increases the downward pressure on the stock, increasing dilution. Some financing vehicles are structured to augment this process by redefining the conversion factor as the stock price declines, thus leading to a "death spiral".

Impact of options and warrants dilution

Options and warrants are converted at pre-defined rates. As the stock price increases, their value increases dollar-for-dollar. If the stock is valued at a stable price-to-earnings ratio (P/E) it can be predicted that the options' rate of increase in value will be 20 times (when P/E=20) the rate of increase in earnings. The calculation of "what percentage share of future earnings increases goes to the holders of options instead of shareholders?" is

- (in-the-money options outstanding as % total) * (P/E ratio) = % future earnings accrue to option holders

For example, if the options outstanding equals 5% of the issued shares and the P/E=20, then 95% (= 5/105*20) of any increase in earnings goes, not to the shareholders, but to the options holders.

A share dilution scam happens when a company, typically traded in unregulated markets such as the OTC Bulletin Board and the Pink Sheets, repeatedly issues a massive number of shares into the market (using follow-on offerings) for no particular reason, considerably devaluing share prices until they become almost worthless, causing huge losses to shareholders.

Then, after share prices are at or near the minimum price a stock can trade and the share float has increased to an unsustainable level, those fraudulent companies tend to reverse split and continue repeating the same scheme.

Investor-backed private companies and startups

Stock dilution has special relevance to investor-backed private companies and startups. Significantly dilutive events occur much more frequently for private companies than they do for public companies. These events happen because private companies frequently issue large amounts of new stock every time they raise money from investors.

Private company investors often acquire large ownership stakes (20%-35%) and invest large sums of money as part of the venture capital process. To accommodate this, private companies must issue large amounts of stock to these investors. The issuance of stock to new investors creates significant dilution for founders and existing shareholders.

Company founders start with 100% ownership of their company but frequently have less than 35% ownership in the later-stages of their companies' life cycles (i.e., before a sale of the company or an IPO). While founders and investors both understand this dilution, managing it and minimizing it can often be the difference between a successful outcome for founders and a failure. As such, dilutive terms are heavily negotiated in venture capital deals.

Share capital

A corporation's share capital (or capital stock in US English) is the portion of a corporation's equity that has been obtained by the issue of shares in the corporation to a shareholder, usually for cash.

In a strict accounting sense, share capital is the nominal value of issued shares (that is, the sum of their par values, as indicated on share certificates). If the allocation price of shares is greater than their par value, e.g. as in a rights issue, the shares are said to be sold at a premium (variously called share premium, additional paid-in capital or paid-in capital in excess of par). Commonly, the share capital is the total of the aforementioned nominal share capital and the premium share capital. Conversely, when shares are issued below par, they are said to be issued at a discount or part-paid.

Sometimes shares are allocated in exchange for non-cash consideration, most commonly when company A acquires company B for shares. Here the share capital is increased to the par value of the new shares, and the merger reserve is increased to the balance of the price of company B.

Besides its meaning in accounting, described above, "share capital" may also describe the number and types of shares that compose a company's share structure. For an example of the different meanings: a company might have an "outstanding share capital" of 500,000 shares (the "structure" usage); it has received for them a total of 2 million dollars, which in the balance sheet is the "share capital" (the accounting usage).

The legal aspects of share capital are mostly dealt with in a jurisdiction's corporate law system. An example of such an issue is that when a company allocates new shares, it must do so in a way that does not inequitably dilute existing shareholders without their agreement.

![[pics]Her Dress Made People Go Nuts On The Red Carpet, People Couldn’t Stop Staring](https://images.outbrainimg.com/transform/v3/eyJpdSI6ImFhMDVjOGQ5NGQ2MDAyYmIwZDkzYjg0NGE1ZjRkNTMyOGFlNGQ3ZWMxZjQyYzY3NmY4NzBhMTg5MTM2ZTBjZWIiLCJ3IjoyNDAsImgiOjE2MCwiZCI6MS41LCJjcyI6MCwiZiI6MH0.webp)

Legal capital

Legal capital is a concept used in UK company law, EU company law, and various other corporate law jurisdictions to refer to the sum of assets contributed to a company by shareholders when they are issued shares. The law often requires that this capital is maintained, and that dividends are not paid when a company is not showing a profit above the level of historically recorded legal capital.

In the UK a public limited company must have a minimum legal capital of £50,000. There is no such requirement for a private company.

XO___XO XXX EXPLANATION OF HOW MONEY MOVES AROUND THE BANKING SYSTEM

Twitter went mad last week because somebody had transferred almost $150m in a single Bitcoin transaction. This tweet was typical:

194,993 BTC transaction worth $147m sparks mystery and speculation coinde.sk/18eil43

There was much comment about how expensive or difficult this would have been in the regular banking system – and this could well be true. But it also highlighted another point: in my expecience, almost nobody actually understands how payment systems work. That is: if you “wire” funds to a supplier or “make a payment” to a friend, how does the money get from your account to theirs?

In this article, I hope to change this situation by giving a very simple, but hopefully not oversimplified, survey of the landscape.

First, let’s establish some common ground

Perhaps the most important thing we need to realise about bank deposits is that they are liabilities. When you pay money into a bank, you don’t really have a deposit. There isn’t a pot of money sitting somewhere with your name on it. Instead, you have lent that money to the bank. They owe it to you. It becomes one of their liabilities. That’s why we say our accounts are in credit: we have extended credit to the bank. Similarly, if you are overdrawn and owe money to the bank, that becomes your liability and their asset. To understand what is going on when money moves around, it’s important to realise that every account balance can be seen in these two ways.

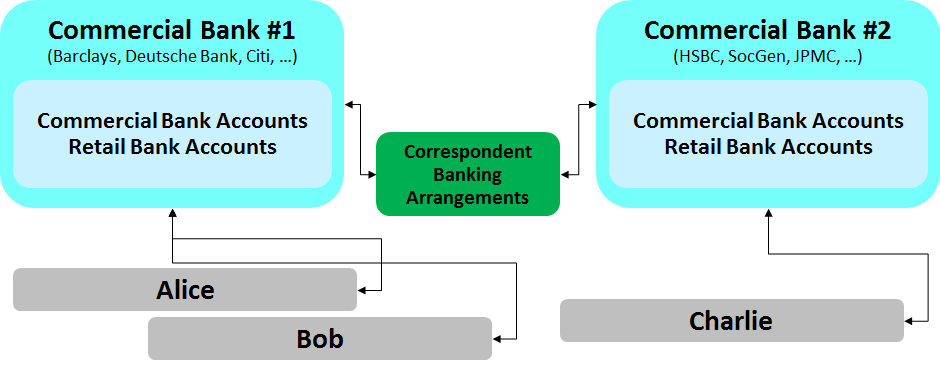

Paying somebody with an account at the same bank

Let’s start with the easy example. Imagine you’re Alice and you bank with, say, Barclays. You owe £10 to a friend, Bob, who also uses Barclays. Paying Bob is easy: you tell the bank what you want to do, they debit the funds from your account and credit £10 to your friend’s account. It’s all done electronically on Barclays’ core banking system and it’s all rather simple: no money enters or leaves the bank; it’s just an update to their accounting system. They owe you £10 less and owe Bob £10 more. It all balances out and it’s all done inside the bank: we can say that the transaction is “settled” on the books of your bank. We can represent this graphically below: the only parties involved are you, Bob and Barclays. (The same analysis, of course, works if you’re a Euro customer of Deutsche Bank or a Dollar customer of Citi, etc)

But what happens if you need to pay somebody at a different bank?

This is where it get more interesting. Imagine you need to pay Charlie, who banks with HSBC. Now we have a problem: it’s easy for Barclays to reduce your balance by £10 but how do they persuade HSBC to increase Charlie’s balance by £10? Why would HSBC be interested in agreeing to owe Charlie more money than they did before? They’re not a charity! The answer, of course, is that if we want HSBC to owe Charlie a little more, they need to owe somebody else a little less.

Who should this “somebody else” be? It can’t be Alice: Alice doesn’t have a relationship with HSBC, remember. By a process of elimination, the only other party around is Barclays. And here is the first “a ha” moment… what if HSBC held a bank account with Barclays and Barclays held a bank account with HSBC? They could hold balances with each other and adjust them to make everything work out…

Here’s what you could do:

- Barclays could reduce Alice’s balance by £10

- Barclays could then add £10 to the account HSBC holds with Barclays

- Barclays could then send a message to HSBC telling them that they had increased their balance by £10 and would like them, in turn, to increase Charlie’s balance by £10

- HSBC would receive the message and, safe in the knowledge they had an extra £10 on deposit with Barclays, could increase Charlie’s balance.

It all balances out for Alice and Charlie… Alice has £10 less and Charlie has £10 more.

And it all balances out for Barclays and HSBC. Previously, Barclays owed £10 to Alice, now it owes £10 to HSBC. Previously, HSBC was flat, now it owes £10 to Charlie and is owed £10 by Barclays.

This model of payment processing (and its more complicated forms) is known as correspondent banking. Graphically, it might look like the diagram below. This builds on the previous diagram and adds the second commercial bank and highlights that the existence of a correspondent banking arrangement allows them to facilitate payments between their respective customers.

This works pretty well, but it has some problems:

- Most obviously, it only works if the two banks have a direct relationship with each other. If they don’t, you either can’t make the payment or need to route it through a third (or fourth!) bank until you can complete a path from A to B. This clearly drives up cost and complexity. (Some commentators restrict the use of the term “correspondent banking” to this scenario or scenarios that involve difference currencies but I think it helpful to use the term even for the simpler case)

- More worryingly, it is also risky. Look at the situation from HSBC’s perspective. As a result of this payment, their exposure to Barclays has just increased. In our example, it is only by £10. But imagine it was £150m and the correspondent wasn’t Barclays but was a smaller, perhaps riskier outfit: HSBC would have a big problem on its hands if that bank went bust. One way round this is to alter the model slightly: rather than Barclays crediting HSBC’s account, Barclays could ask HSBC to debit the account it maintains for Barclays. That way, large inter-bank balances might not build up. However, there are other issues with that approach and, either way, the interconnectedness inherent in this model is a very real problem.

We’ll work through some of these issues in the following sections.

[Note: this isn’t *actually* what happens today because the systems below are used instead but I think it’s helpful to set up the story this way so we can build up an intuition for what’s going on]

Hang on… why are you making this so complicated? Can’t you just say “SWIFT” and be done with it?

It is common when discussing payment systems to have somebody wave their hands, shout “SWIFT” and believe they’ve settled the debate. To me, this just highlights that they probably don’t know what they’re talking about

The SWIFT network exists to allow banks securely to exchange electronic messages with each other. One of the message types supported by the SWIFT network is MT103. The MT103 message enables one bank to instruct another bank to credit the account of one of their customers, debiting the account held by the sending institution with the receiving bank to balance everything out. You could imagine an MT103 being used to implement the scenario I discussed in the previous section.

So, the effect of a SWIFT MT103 is to “send” money between the two banks but it’s critically important to realise what is going on under the covers: the SWIFT message is merely the instruction: the movement of funds is done by debiting and crediting several accounts at each institution and relies on banks maintaining accounts with each other (either directly or through intermediary banks). Simply waving one’s hands and shouting “SWIFT” serves to mask this complexity and so impedes understanding.

OK… I get it. But what about ACH and EURO1 and Faster Payments and BACS and CHAPS and FedWire and Target2 and and and????

Slow down….. Let’s recap first.

We’ve shown that transferring money between two account holders at the same bank is trivial.

We’ve also shown how you can send money between account holders of different banks through a really clever trick: arrange for the banks to hold accounts with each other.

We’ve also discussed how electronic messaging networks like SWIFT can be used to manage the flow of information between banks to make sure these transfers occur quickly, reliably and at modest cost.

But we still have further to go… because there are some big problems: counterparty risk, liquidity and cost.

The two we’ll tackle first are liquidity and cost

We need to address the liquidity and cost problem

First, we need to acknowledge that SWIFT is not cheap. If Barclays had to send a SWIFT message to HSBC every time you wanted to pay £10 to Charlie, you would soon notice some hefty charges on your statement. But, worse, there’s a much bigger problem: liquidity.

Think about how much money Barclays would need to have tied up at all its correspondent banks every day if the system I outlined above were used in practice. They would need to maintain sizeable balances at all the other banks just in case one of their customers wanted to send money to a recipient at HSBC or Lloyds or Co-op or wherever. This is cash that could be invested or lent or otherwise put to work.

But there’s a really nice insight we can make: on balance, it’s probably just as likely that a Barclays customer will be sending money to an HSBC customer as it is that an HSBC customer will be sending money to a Barclays customer on any given day.

So what if we kept track of all the various payments during the day and only settled the balance?

If you adopted this approach, each bank could get away with holding a whole lot less cash on deposit at all its correspondents and they could put their money to work more effectively, driving down their costs and (hopefully) passing on some of it to you. This thought process motivated the creation of deferred net settlement systems. In the UK, BACS is such a system and equivalents exist all over the world. In these systems, messages are not exchanged over SWIFT. Instead, messages (or files) are sent to a central “clearing” system (such as BACS), which keeps track of all the payments, and then, on some schedule, calculates the net amount owed by each bank to each other. They then settle amongst themselves (perhaps by transferring money to/from the accounts they hold with each other) or by using the RTGS system described below.

This dramatically cuts down on cost and liquidity demands and adds an extra box to our picture:

It’s worth noting that we can also describe the credit card schemes and even PayPal as Deferred Net Settlement systems: they are all characterised by a process of internal aggregation of transactions, with only the net amounts being settled between the major banks.

But this approach also introduces a potentially worse problem: you have lost settlement finality. You might issue your payment instruction in the morning but the receiving bank doesn’t receive the (net) funds until later. The receiving bank therefore has to wait until they receive the (net) settlement, just in case the sending bank goes bust in the interim: it would be imprudent to release funds to the receiving customer before then. This introduces a delay.

The alternative would be to take the risk but reverse the transaction in the event of a problem – but then the settlement couldn’t in any way be considered “final” and so the recipient couldn’t rely on the funds until later in any case.

Can we achieve both Settlement Finality and Zero Counterparty Risk?

This is where the final piece of the jigsaw fits in. None of the approaches we’ve outlined so far are really acceptable for situations when you need to be absolutely sure the payment will be made quickly and can’t be reversed, even if the sending bank subsequently goes bust. You really, really need this assurance, for example, if you’re going to build a securities settlement system: nobody is going to release $150m of bonds or shares if there’s a chance the $150m won’t settle or could be reversed!

What is needed is a system like the first one we outlined (Alice pays Bob at the same bank) – because it’s really quick – but which works when more than one bank is involved. The multilateral bank-bank system outlined above sort-ofworks but gets really tricky when the amounts involved get big and when there’s the possibility that one or other of them could go bust.

If only the banks could all hold accounts with a bank that cannot itself go bust… some sort of bank that sat in the middle of the system. We could give it a name. We could call it a central bank!

And this thought process motivates the idea of a Real-Time Gross Settlement system.

If the major banks in a country all hold accounts with the central bank then they can move money between themselves simply by instructing the central bank to debit one account and credit the other. And that’s what CHAPS, FedWire and Target 2 exist to do, for the Pound, Dollar and Euro, respectively. They are systems that allow real-time movements of funds between accounts held by banks at their respective central bank.

- Real Time – happens instantly.

- Gross – no netting (otherwise it couldn’t be instant)

- Settlement – with finality; no reversals

This completes our picture:

something to do with Bitcoin?

can we place Bitcoin on this model?

My take is that the Bitcoin network most closely resembles a Real-Time Gross Settlement system. There is no netting, there are (clearly) no correspondent banking relationships and we have settlement, gross, with finality.

But the interesting thing about today’s “traditional” financial landscape is that most retail transactions are not performed over the RTGS. For example, person-to-person electronic payments in the UK go over the Faster Payments system, which settles net several times per day, not instantly. Why is this? I would argue it is primarily because FPS is (almost) free, whereas CHAPS payments cost about £25. Most consumers probably would use an RTGS if it were just as convenient and just as cheap.

So the unanswered question in my mind is: will the Bitcoin payment network end up resembling a traditional RTGS, only handling high-value transfers? Or will advances in the core network (block size limits, micropayment channels, etc) occur quickly enough to keep up with increasing transaction volumes in order to allow it to remain an affordable system both for large- and low-value payments?

My take is that the jury is still out: I am convinced that Bitcoin will change the world but I’m altogether less convinced that we’ll end up in a world where every Bitcoin transaction is “cleared” over the Blockchain.

NEW MODELS FOR UTILITY TOKENS

There are three types of cryptoassets: stores of value, security tokens, and utility tokens. General-purpose stores of value should be valued using the equation of exchange because these currencies are independent monetary bases. Examples include Bitcoin, Bitcoin Cash, Zcash, Dash, Monero, and Decred.

Although some may disagree, I also include the native tokens of smart contract platforms such as Ethereum, EOS, Dfinity, and Kadena in this category. Why? Because there’s a real chance that the native token of a smart contract platform that becomes sufficiently useful will emerge as an independent store of value.

I won’t touch on security tokens in this essay as traditional securities are widely understood. Moving securities onto a blockchain, while better than legacy systems in terms of settlement times and custodianship, doesn’t change anything about the nature of the security itself.

This essay will focus on utility tokens.

Background

The vast majority of ICOs that launched in 2016 and 2017 were utility tokens that also acted as proprietary payment currencies. These include many of the highest-profile projects: Filecoin, Golem, 0x, Civic, Raiden, Basic Attention Token, and more.

Each of these cryptocurrencies is presenting itself as a freestanding monetary base. Monetary bases should be valued using the equation of exchange: MV = PQ. Therefore M = PQ/V.

As I noted in Understanding Token Velocity, the V in the equation of exchange is a huge problem for basically all proprietary payment currencies. Proprietary payment currencies are, generally speaking, susceptible to the velocity problem, which will exert perpetual downwards price pressure. Due to this effect, I expect to see utility tokens that are just proprietary payment currencies exceed a velocity of 100. Velocities of 1,000 are even possible. As a point of reference, the USD M1 supply has a velocity of 5.5.

Below I’ll present two new token economic models that address the velocity problem for utility tokens. Both models are primarily designed to optimize for the following:

The price of the utility token should increase approximately linearly with usage of the network.

Of course, the corollary to this is that the price of the native token should decrease if usage of the network falls, or grows more slowly than previously forecast.

Work Tokens

In the work token model, a service provider stakes (AKA bonding) the native token of the network to earn the right to perform work for the network. For services which are commodities such as Keep (off-chain private computation), Filecoin (distributed file storage), Livepeer (distributed video encoding), Truebit (off-chain verifiable computation), and even “decentralized mechanical Turk” powered by humans such as Gems, the probability that a given service provider is awarded the next job is proportional to the number of tokens staked as a fraction of total tokens staked by all service providers.

The beauty of the work token model is that, absent any speculators, increased usage of the network will cause an increase in the price of the token. As demand for the service grows, more revenue will flow to service providers. Given a fixed supply of tokens, service providers will rationally pay more per token for the right to earn part of a growing cash flow stream.

Most work tokens systems enforce some sort of mechanism to penalize workers who fail to perform their job to some pre-specified standard. For example, in Filecoin, service providers contractually commit to storing some data for a period of time. During the life of the contract, service providers must lock up some number of Filecoin, and the file must be available 24/7 with some minimum bandwidth guarantee. If the service provider does not adhere to this standard, she’s automatically penalized by the protocol, and some of her staked tokens are slashed (taken away).

Relative to the traditional “tokens as money” model, the work token model completely changes the terminal value calculation of a utility token. Let’s consider Filecoin to highlight the magnitude of the discrepancy.

The Filecoin team has suggested that their target market is $110B (page 16) in 2021. These figures are based on the legacy model of buying hard drives with the express intent of renting them out, rather than leveraging what is otherwise unused capacity. Filecoin is likely to offer to substantially lower unit prices. Let’s be conservative and assume that Filecoin doesn’t reduce prices at all.

Filecoin, using the “token as money” model, will have a high velocity. The velocity will not approach infinity—there is an upper limit because storage providers in the Filecoin network must post a deposit before storing files. The exact mechanics of this staking system are not yet set. Regardless, this mechanism guarantees some upper bound on the velocity of Filecoin tokens (similarly, transaction fees also impose some upper bound; however, that upper bound is likely to be so high as to be irrelevant in the context of this essay).

The velocity of the USD M1 is about 5.5. Prior to the financial crisis (in which the Federal Reserve approximately doubled the money supply), the velocity was about 10. But 10 isn’t a realistic assumption for Filecoin. Given that Filecoin isn’t intended to be general-purpose money, and that there’s not a compelling motivation to hold Filecoin beyond the minimum staking requirements, I’ll assume 3-10x higher velocity than USD M1. This implies a velocity of 30-100.

The terminal value for Filecoin—assuming 100% market saturation— is therefore somewhere in the range of $1.1B-$3.6B ($110B/100 and $110B/30).

Now, let’s consider Filecoin’s potential terminal value in the work token model. Terminal value can be calculated as cash flow / discount rate. Assuming a discount rate of 40% and operating margins of 50%*, the potential terminal value of Filecoin is $110B x 50% / 40% = $137.5B.

The work token model captures ~100x more value than the proprietary payment currency model.

How is this possible?

Considering utility tokens as a proprietary payment currency, terminal value will trend towards a value that’s a fraction of transaction volume. Why? Because, per the equation of exchange, M = PQ/V, and assuming a V > 1, M must be less than PQ.

On the other hand, if you instead use a utility token as a right to perform work on behalf of the network, it becomes valued at a multiple of the operating cash flows that the system generates rather than as a fraction of revenues paid to service providers**. Moreover, in the work token model, as a network grows and matures, it will de-risk, decreasing the discount rate, and ultimately increasing the terminal value (this actually implies that total token value should grow super-linearly relative to transaction throughput).

The work token model only works if the service being provided is a pure commodity. If suppliers compete on other variables, such as marketing, customer service, go-to-market strategies, etc. then the work token model doesn’t work. The work-token model is predicated on assigning new jobs to service providers based on their staked tokens. This is not amenable to service providers who must actively compete for customers. In these types of networks, another model is necessary.

Burn-And-Mint Equilibrium

Factom is the pioneer of the burn-and-mint equilibrium (BME) model, and is to the best of my knowledge the only token with a substantial network value that implements this model. (Factom is providing a commodity service that could be implemented as a work token; however, they chose to implement BME instead.)

In the BME model, unlike the work token model, tokens are a proprietary payment currency. But unlike traditional proprietary payment currencies, users who want to use a service do not directly pay a counterparty to use the service. Rather, users burn tokens.

Yes, the customer burns the money.

When the customer burns the money, they do so in the name of the service provider. That is, the customer publicly acknowledges (on chain) that the service provider did the work for the money that was burned.

The amount of token burned to access the underlying service should be denominated in USD. For example, in Factom, the cost of committing an entry to the Factom blockchain is $.001, regardless of the price of Factoids (FCT) in USD.

Independently of the token burning process, the protocol should mint X new tokens per time period, and allocate those tokens to service providers ratably: If 1 of 50 tokens burned during a token minting period were in the name of Service Provider A, then Service Provider A should receive 2% of newly minted tokens.

Note that X does not have to be static. It can be variable, so long as X is not a function of burned tokens (this would create circular logic, and ultimately defeat the purpose of BME).

On the surface, it seems like this model could create scenarios in which service providers are under or overpaid. However, in practice, if the system is running near equilibrium state, then service providers will be paid the appropriate amount.

Also note that in the case of Factom, service providers and block producers are the same. For ERC20 tokens, this is by definition not true since the Ethereum network abstracts block production. However, the BME model can be adopted for ERC20 tokens.

Like the work token model, the BME model creates a model in which linear growth in usage of the network causes linear, non-speculative growth in the value of the token.

Let’s walk through an example that assumes no market speculators. I’ll assume the following:

Tokens minted per month: 10,000

Cost of token in USD: $10.00

Unit cost of service: $.001

The system will be in equilibrium—meaning that the number of tokens in circulation remains unchanged— if 10,000 tokens are burned per month. Since the cost of using the service is $.001, the system will be in equilibrium if the service is used (10,000 * 10)/.001 = 100,000,000 times per month. If usage grows and 15,000 tokens are burned in a month, then total supply will decrease, creating upwards price pressure. This upwards price pressure means fewer tokens need to be burned to purchase the same amount of service from the network, bringing the system back into equilibrium.

The same system works in reverse: If usage slows and more tokens are minted than burned in a given month, supply increases, creating downwards price pressure, meaning more tokens have to be burned for the same amount of service, bringing the system back to equilibrium.

This model assumes that both consumers and service providers never want to actually hold the proprietary payment currency. Rather, this model assumes that service providers only want to hold general purpose currencies.

Note that this model doesn’t require that the service being provided is a commodity. The ratable redistribution of newly minted tokens allows service providers to price their service however they see fit.

Given that there will always be excess supply floating in the market as Menger Goods, there isn’t a universal formula model that can be used to calculate non-speculative value. Regardless, the following can be generalized:

Price should increase if # of tokens burned > # of tokens of minted

Price should decrease if # of tokens burned < # of tokens of minted

When To Use Each Model

Given that work tokens capture far more value than BME tokens, teams should try to implement work tokens whenever possible. However, the work token is not universally applicable. Work tokens are applicable for most decentralized cloud services such as Filecoin, Keep, Truebit, and Livepeer. These services can use the work token model because they provide undifferentiated commodity services. Additionally, work tokens can be used for services that require human input such as Augur or Gems.

Even systems like Filecoin that offer different levels of service—e.g., amount of redundancy—can adopt the work token model.

Most other services should use the BME model: Civic, Golem, Raiden, Basic Attention Token (BAT), 0x, etc. In these models, service providers aren’t providing a pure commodity. They’re competing on variables that are out of band relative to the protocol itself. Service providers on the Civic network compete on business development and partnership development. 0x relayers compete on UX, quality of API, SLAs, tokens listed, and more. Web publishers compete on differentiated content in the BAT network.

ICOs and Token Distribution

For tokens that employ the work token model, development teams don’t really need to worry about token distribution. Why? Because end users don’t ever need to purchase the token. Service providers seeking yield on underutilized computing/storage/bandwidth resources will figure out how to make money on underutilized hardware relatively quickly. Services like AwesomeMiner will emerge for work token-based staking protocols that dynamically allocate one’s resources to the most profitable network. 1protocol is already working on this.

Unfortunately, the BME model doesn’t provide this same benefit. Systems that implement the BME model will still need to get their tokens in the hands of millions of people so that end users can use the service.

Pricing (Of Services)

In systems using work-tokens, the unit price of the service needs to be set at the network level. Individual service providers cannot set pricing. Relative to the free-market approach of Filecoin (every miner sets her own price in a hyper-competitive market), this sounds worse. However, in practice, there will be competition, not between providers in the same network, but among providers across different networks. This is similar to how Amazon and Google set prices for storing 1GB of data in their respective cloud offerings.

In systems implementing BME, every service provider can set her own price.

Governance

For tokens that implement the generic “tokens as money” model, many entrepreneurs assume that users will have a say in governance. This is unlikely to be true in practice. Because of the velocity problem, consumers won’t hold tokens, so they’re unlikely to vote in stake-based governance models. Why spend time voting on governance issues when you only intend to hold the token for ten seconds at a time?

The work token model embraces this truth by moving stake-based voting exclusively to the supply side of the market. This feels a lot more like decentralized equity in the sense that traditional equity holders vote on what the company (supply side) should do in the context of a competitive marketplace.

In the BME model, tokens are still acting as money. It’s unclear how the BME will impact stake-based voting governance, if at all, relative to the proprietary payment currencies that don’t implement BME.

Network Effects

Neither of these models should materially affect network effects relative to the generic “tokens as money” model. Network effects for utility tokens are not based on liquidity of the token itself. They’re based on the intrinsic nature of the protocol. For example, the network effect in 0x isn’t the liquidity between ETH and ZRX, but rather the network effect of the global liquidity pool of all trading pairs using the 0x protocol. If ZRX tokens adopt the BME model, the global liquidity pool will remain unchanged. Similarly, the network effect of Filecoin, which should be approximately log(n) (due to decreasing value per marginal miner as you approach global saturation), should not be materially different as a work token versus proprietary payment currency.

Scaling Work Token Networks

In the work token model, some interesting phenomena emerge as the network grows in usage and value.

Let’s say that at time of network launch, I own 1% of all Keep tokens, that the entire Keep network can be powered by 300 mid-range AWS servers, and that there are no market speculators. In order to perform this work, I need 3 mid-range AWS servers. Let’s then say that, over the next year, demand for Keep tokens grows 100x, and that I don’t sell any tokens. In order to service that demand I’ll need to manage 300 servers.

But I don’t want to manage 300 servers. That’s just too complicated for me.

What now? I can just sell my tokens on the open market. The market should rationally value the tokens at 100x what they were valued at a year ago, because the cash flows going through the network are 100x what they were a year ago.

If the network grows faster than I can grow as a service provider, that’s ok. I can just sell my tokens to someone else. I may even be able to lend out my tokens to someone else by using 1protocol or something similar.

Synthetic Tokens

Nothing about either of these models assumes that a given token exists on a single smart contract platform. Both the work token and BME models are compatible with synthetic tokens that live across chains as described in The Smart Contract Network Effect Fallacy.

Conclusion

For the first time, Ethereum provides a canvas for developers, service providers, and consumers to transact using programmable money. Work tokens and the BME model are just two examples of the opportunities created by programmable money. The design space for programmable money is wide open and totally unexplored. New models and mechanics will emerge.

As the crypto ecosystem matures, developers will experiment, tweaking and building on the ideas presented in this essay. As they do, they’ll find new and creative ways to capture value in the native tokens of their networks without degrading user experience.

Lastly, I welcome your feedback. Please email research@multicoin.capital with questions and ideas. I presented a tremendous amount of material in this essay. I look forward to learning from the public and iterating on the ideas and designs presented in this essay.

Thanks to Matt Luongo and James Prestwich (Keep), Doug Petkanics and Eric Tang (Livepeer), Jon Choi (Ethereum Foundation), Will Peets (Passport Capital), Matt Huang (Sequoia), Gustav Simonsson (Orchid), and the others who provided input on this essay.

Update – April 18th, 2018

Doug Petkanics of Livepeer has proposed a solution to adding price discovery to the work token model:

1. Protocol progresses in rounds.

2. Worker nodes advertise their price for some unit of work, which will get locked in during the next round.

3. During the final X% of a round (say 10%), the minimum price offered by any worker node is locked in, and the only price change allowed for other worker nodes is downward adjustment in price up to this minimum amount. The effect of this is that all nodes have the option of matching the minimum offered price.

4. Users offer the maximum price they’re willing to pay. All worker nodes who have offered a price <= this offered price are considered for the job, and work is distributed to them in proportion to stake.

2. Worker nodes advertise their price for some unit of work, which will get locked in during the next round.

3. During the final X% of a round (say 10%), the minimum price offered by any worker node is locked in, and the only price change allowed for other worker nodes is downward adjustment in price up to this minimum amount. The effect of this is that all nodes have the option of matching the minimum offered price.

4. Users offer the maximum price they’re willing to pay. All worker nodes who have offered a price <= this offered price are considered for the job, and work is distributed to them in proportion to stake.

Since nodes had the option of matching the minimum price, they are essentially opting in to work distributed in proportion to stake. But if that price is too low for them to operate profitably, then they’ll likely converge on the 2nd lowest, or 3rd lowest price. At this point the network risks capacity planning issues…where users may all offer only the lowest possible price…except a single or very few nodes at that price won’t be able to handle the full capacity. This is a different problem which is also solve-able but a little complex to implement. The capacity issues could just be puntable to the users…who will determine through observation that they need to offer a higher price for their job to be picked up and completed in short order.

End Notes